Suits

Last month, Shefi touched on the topic of deep generalists and why the insurance industry needs them. My background is in marketing and the first step in marketing is to learn about the product, consumer, and landscape. Essentially, marketing is the practice of generalism. I view myself as a generalist and because of Shefi’s insurance expertise, I was forced to go down the (insurance) rabbit hole. I like to believe that I had a similar impact on her, after all, she is the one behind Insurance Under the Influence® – the generalist approach for understanding and responding to challenges and opportunities related to insurance.

Unlike a specialist who is an expert on a specific subject matter, a generalist is someone who’s able to find inspiration from other areas. When Aureus needed help with marketing, I put my generalist hat on and realized how their solution can significantly reduce the time I spend reading restaurant reviews on Yelp. So, we created The Aureus Analytics Las Vegas Restaurant Guide for ITC 2019 because (1) they were attending the conference and I figured (2) others would appreciate the effort. The guide featured a variety of insights – for example, we counted the average words per review for each restaurant as we believed that people who took the time to write more had a stronger experience. We’ve also looked at the number of exclamation marks in positive and negative reviews because some know that exclamation marks shouldn’t be used lightly.

While we spent a considerable amount of time in the U.S., both Shefi and I are Israelis, and Israel is a country that emphasizes responsible consumption. For example, we were taught at a young age to turn off the water while brushing our teeth. Another example is the limited supply of hot water as it would entail a high electricity bill. Growing up in this kind of environment has shaped our thinking and our Coffee Coverage campaign idea (way before Domino’s Carryout Insurance or Progressive’s Turkey Insurance) is a great example of that – we wanted to find a cost-effective way to advertise insurance. If Prudential had consulted us before buying Assurance IQ, we would have told them that if they were serious about getting into this market, it would be cheaper to invest $136 million (the sum Assurance IQ has lost over the last six quarters) in their own venture and fail, saving the $2.35 billion they paid for the company.

Whenever a company highlights the number of years they’ve been in business, you know you’re dealing with a specialist. On its About page, Prudential writes that they’ve been helping individual and institutional customers grow and protect their wealth for over 140 years. This specialist mentality is what drove the company to look for a VP with a strong knowledge of the annuities industry who among other things will need to “identify new breakthrough business models (e.g. FinTech/Insurtech) that present potential disruption and growth opportunities for Annuities.” A smarter move would have been to look for a generalist who knows just enough about fintech and annuities to recognize that one screams ‘modern’ while the other screams ‘legacy’.

Fintech darling Chime surpassed 8 million accounts in February 2020. Its average customer is between 25 and 35 and spends over $1,000 a month with the Chime debit card. The startup, which raised ~$1.5 billion and was last valued at $14.5 billion, is known for its simple and straightforward approach to banking. On the other hand, Prudential features 8 annuity products with names as short as 3 words and as long as 8, all of which carry the ® or ℠ symbols, of course. When you sell yourself as a specialist, you benefit from making things complicated.

Technicalities aside, one company is riding this generational wave while the other is yelling at people to get out of the water with its suit on. “Chime’s business was built on the principle of protecting our members and helping them get ahead,” the company states on its About page. “That means we don’t profit off of you. We profit with you: every time you use your Chime debit card, we earn a small amount from Visa (paid by the merchant).” And just like that Prudential and others are seen as the old bad guys looking to profit off of financially stressed individuals.

When you’re a specialist you immerse yourself in your specific field to that point where you may become blind, even to internal signals. For months and months, Keith Gill, aka Roaring Kitty, was working at MassMutual’s securities and investment advisory business as a director of financial wellness education while also educating redditors about GameStop and investing without charging a fee.

Folks like Gill, and the Kardatzke brothers who built Quiver Quantitative to help “the little guys” get access to alternative data usually reserved to hedge funds, helped create the so-called “Reddit Rally” which surfaced more and more messages of this nature:

(1) “Be your own tendies manager…I think that’s where this all started tbh. Giving your money to someone to manage/invest is a legacy mindset we were taught, but I think is fundamentally wrong. (Same goes for 401k IMO) I don’t need anyone to manage my money. I can’t bring myself to believe someone else can make better decisions with my money for what is best for my life. I had a financial advisor and he did nothing but take commission from me for decisions that didn’t reflect anything close to the path I wanted to be on. Fired him and took control myself and have done exponentially better. Not to mention it has brought me here. Just my thoughts. Buy/hold create your own success. Don’t rely on anyone else to make good decisions for you.”

(2) “Financial advisory is a relic of an age where information was not so easily distributed and certainly not so decentralized. It has taken only three months for a rowdy squad of howling and chattering apes of all shapes to hack together a bootleg alternative to the Bloomberg terminal that costs 24,000 less dollars a year to use; review and analyze a genuinely silly amount of sec filings and self-regulatory organization rule amendment proposal; provide valuable education on financial literacy to a growing audience; naturally, evolve into a news outlet with an emphasis on drawing attention to conspicuously unreported financial news and begin to show the characteristics of a vast and volunteer-backed consensus watchdog report.

This of course comes with the caveat – when information becomes so widely available how can you tell what/who you can trust? I think that the education on critical thinking skills recently has helped on that front as well. my only two problems with the roiling hive mind is that people shouldn’t automatically believe something that confirms their bias before looking at the details and the author themselves, and they shouldn’t immediately reach the conclusion that someone who has a different opinion than them is a shill.

Setting aside those two I think that this is a great example of how the decentralized aggregation, analysis, and dispersal of data can be incredibly useful (despite its vulnerability to malicious or misinformed noise). But to answer the more immediate question I genuinely believe that a community with an emphasis on financial research, fundamental/technical/stochastic analysis and broad investing strategies will emerge from this and live on long after this wild and wacky saga has concluded.”

Today, Reddit’s wallstreetbets account counts 10 million “degenerates” that share the mantra of “apes together strong” and its about section reads the following: “Like 4chan found a Bloomberg Terminal.”

In a recent interview with Robert Anderson of Choice Insurance Agency, we asked him what advice he would give to new insurance agents. His response: “Celebrate Namath and Selleck, along with the offshore call centers, they are doing more to secure your go-to-market than anything GOOD that you could possibly do. Everything in life is relative.” The “everything in life is relative” part stuck with me and after Robinhood went from stealing from the rich to give to the poor to steal from the poor to give to the rich. Public, another commission-free investment app, seized the moment and announced that it will stop participating in Payment for Order Flow and instead introduce optional tipping.

Michelle Obama famously said, “when they go low, we go high.” While this is a noble approach for life, in today’s competitive business environment you need to adopt the “when they go low, we go lower” strategy to stay relevant. Robinhood saw how traditional brokerages try to lure in customers with lower fees so it decided to remove fees altogether. Then came Public and showed that it can go lower than Robinhood’s zero commissions by giving up revenue from Payment for Order Flow and “aligning” itself with the community. More and more businesses are adopting this strategy. Earlier this year, Kyte raised $9 million to offer a delivery and pick up service for car rentals because Enterprise will only pick you up (exclusions apply), and Uber recently introduced Uber Rent with Valet, a car rental service similar to Kyte’s minus the inconvenience of downloading a new app and all that comes with it. And my favorite ‘when they go low we go lower’ move was discovered this week after ordering food on Seamless.

This is an interesting incentive from Seamless+ Their first attempt was 90 days to try the service at no cost. This one includes a free pickup meal ($10) every month. @thenewb pic.twitter.com/rw1bYJIWfC

— Avi Ben-Hutta 🐿 (@FloodQuake) May 4, 2021

The Wall Street Journal is another specialist with a suit telling the world that it has been here almost as long as Prudential. “The Wall Street Journal was founded in July 1889. Ever since the Journal has led the way in chronicling the rise of industries in America and around the world. In no other period of human history has the planet witnessed changes so dramatic or swift. The Journal has covered the births and deaths of tens of thousands of companies; the creation of new industries such as autos, aerospace, oil and entertainment; two world wars and numerous other conflicts; profound advances in science and technology; revolutionary social movements; the rise of consumer economies in the U.S. and abroad; and the fitful march of globalization.”

In a New York Times article titled “Inside the Fight for the Future of The Wall Street Journal,” author Edmund Lee writes that while the U.S. population is growing more racially diverse, older white men still make up the largest chunk of its readership, with retirees a close second. “The No. 1 reason we lose subscribers is they die,” is a joke shared by some Journal editors. This week, News Corp, whose holdings include The Wall Street Journal, reported that the Journal averaged 2.63 million digital subscribers in Q1 2021, up roughly 170,000 from over 2.46 million in Q4 2020. There’s a popular saying in Hebrew that essentially translates to no pain, no gain. According to the Times article, the WSJ is in the process of “pushing for drastic changes” and as we all know change doesn’t happen overnight. So, if we believe the ‘no pain, no gain’ mantra, then perhaps the company’s recent subscriber growth is correlated to this one-day sale that’s apparently been going on for many days ($48 for the year instead of $467).

The world used to be complicated and specialists dominated many fields. Adman Claude Hopkins shared in his book some of the struggles car owners faced in the early days. “I was chauffeur and garage man. It required thirty minutes to start the car, which we had to count on in catching a train. And on more than that. Starting was a small problem when compared with keeping the car going. When we drove ten miles without a breakdown we boasted of the record. When we ever got through to Milwaukee—about twenty-five miles—we went directly to the factory for repairs, and we rarely returned that day.”

The world is simpler today. Allstate’s CEO Tom Wilson discussed this very topic in his company’s recent earnings call. Here are parts of the transcript: “The fast pace of change has all of us on edge, whether you’re a retailer or anybody what’s going on in the world. And good news for our agents is that still, a majority of consumers want an insurance professional [to] help them buy insurance, and our agents are really good at it. That said, people are more comfortable with self-service, simple items, and technology enables a computer to do some of the work that used to be handled in — by people and it still, in some cases, handles an offices. So we have to transition their model and go where the customer is going.”

Wilson wants to take advantage of these simpler times and he prefers that agents focus on the difficult task of selling, while acknowledging that this “new agent model” isn’t for everyone. “If you’ve been focused more on service and not on growth, then you’re not going to be as excited about that change because it changes your business model,” he said. And in the case that encouraging agents to transition to this new model isn’t enough, Wilson is also choosing to discourage shoppers from going with agents – last year Allstate introduced ‘channel of bind’ as a rating variable, instituting a 7% discount for those who buy car insurance online or over the phone rather than through an agent. “We have the direct business, which we’ve launched. And it’s sold, by the way, at a different price than through an agent because we believe customers should pay for what they get. And if you get an agent and get that help, you should be willing to pay for that.”

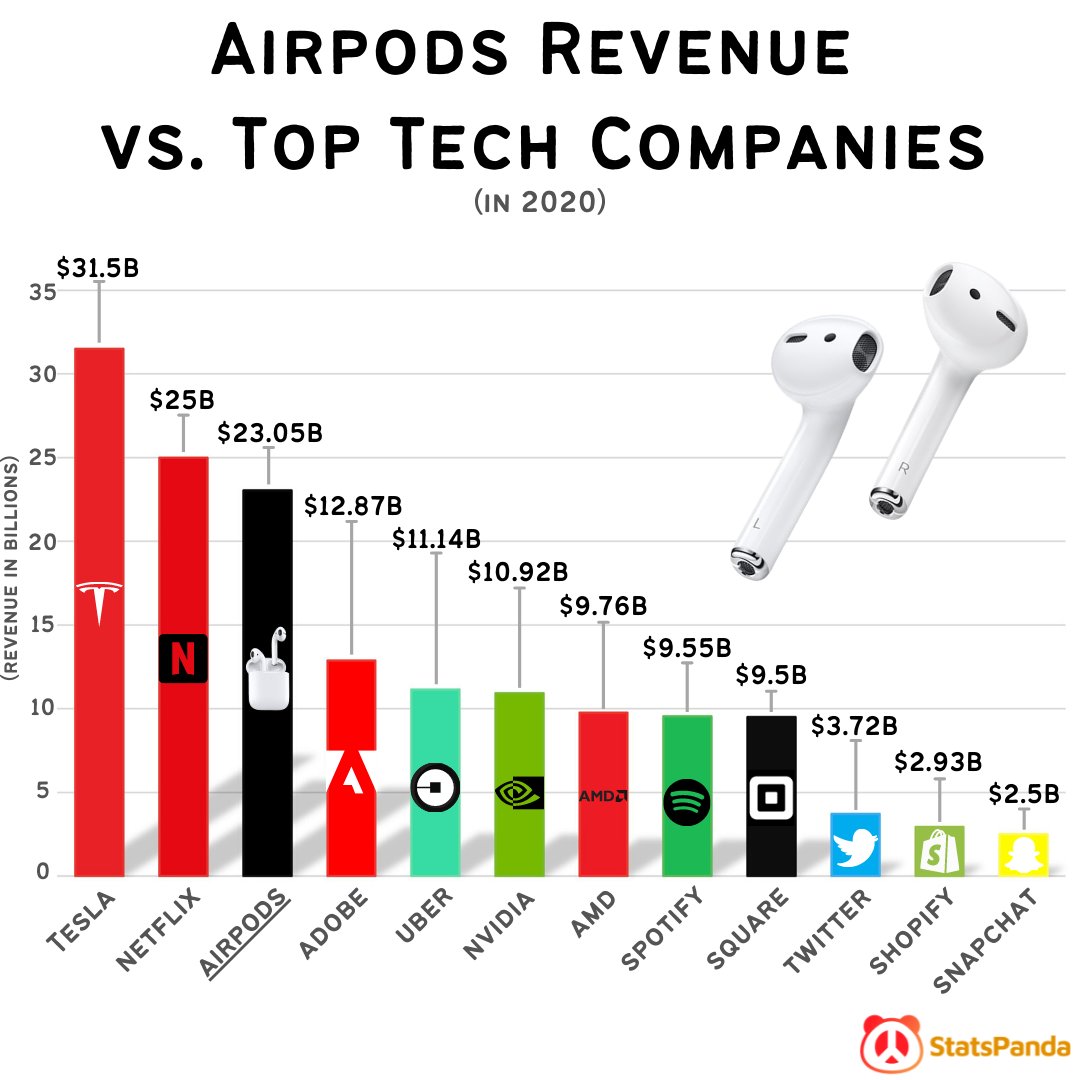

This week, a chart by StatsPanda made waves on Twitter. The chart shows Apple’s Airpods revenue vs. top tech companies.

Apple started with computers and went on to do so much more. Apple is a deep generalist company without an about page because true deep generalists do not define themselves by the past or present. A deep generalist is constantly looking for inspiration from all over and it is time for insurers to do the same.