Lemonade’s Cards

I don’t know Jason Toff personally, but after seeing one of his tweets followed by some research, I can now tell you a few things about him. At 32, Jason Toff is a millennial father and husband living in Hoboken, NJ. Originally from Allentown, PA, Jason attended Parkland High School where he was the Math Club president. After graduating, Jason went on to the University of Pennsylvania but not before he co-founded PALS – an organization that runs summer camps for teens with Down syndrome.

Jason, who now serves as the president of the executive board, helped grow the camp from 16 campers in 2004 to 424 campers in 2017.

https://www.instagram.com/p/BiebIHzl5Yx/?hl=en&taken-by=toff

After college, Jason interned for Josh Kopelman – the founder of First Round Capital, a seed-stage venture fund that led the seed round in Uber. After the internship, Jason joined Google where he served as a product manager in different departments including Gmail, Chrome, Google Voice and YouTube. In 2014, after ~5 years with Google, Jason joined Twitter where he served as the General Manager of Vine, and ~2 years later, he returned to Google where he is now a partner at Area 120 – Google’s workshop for experimental products.

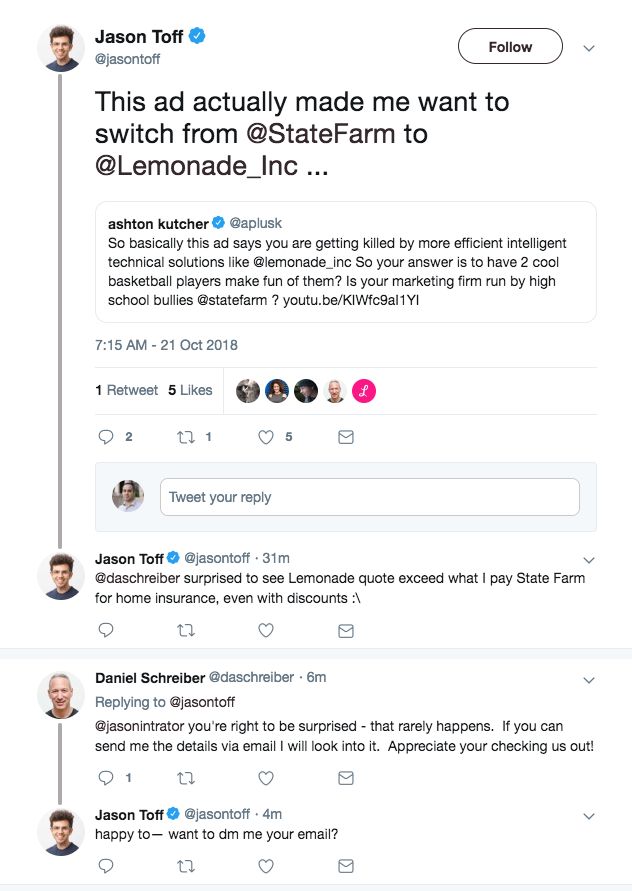

It’s safe to say that Jason has all the characteristics of a Lemonade customer – he’s a millennial, he’s tech-savvy, and he cares about a social cause. Yesterday, while Ashton Kutcher asked State Farm if their marketing firm is managed by “high school bullies” following this commercial, Jason expressed interest in switching from his current home insurer – State Farm, to Lemonade.

This ad actually made me want to switch from @StateFarm to @Lemonade_Inc … https://t.co/ETpUtOrE55

— Jason Toff (@jasontoff) October 21, 2018

But then, something surprising happened. Despite being a tech-savvy, social cause-driven millennial, Jason was surprised to learn that Lemonade’s home insurance quote exceeds his current State Farm premium.

@daschreiber surprised to see Lemonade quote exceed what I pay State Farm for home insurance, even with discounts :

— Jason Toff (@jasontoff) October 21, 2018

And while Jason doesn’t represent all millennials, his tweet is a great wake up call for those under the Lemonade spell . Update: Ashton Kutcher has since removed his original tweet, but here’s a screenshot:

Insurance Isn’t a Poker Game, It’s War

You all know poker, but do you remember war? War is a card game typically played by two players where each player reveals the top card of their deck and the player with the higher card takes both cards. Insurance is like the war card game – some cards (strategies) are stronger than others. And with that in mind, let’s analyze Lemonade’s cards from a business perspective.

The Price Card. This card is probably the most popular and powerful card insurance companies currently use. From “15 minutes can save you 15% or more” to Lemonade’s $5 renters insurance, many companies lead with price. While Lemonade will argue differently, they too mostly lead with price – out of 76 Google ads, 71 contain $5 in the ad copy. Generally speaking, the price card will help you win over most consumers – after all, in a digital (emotionless) world the price card beats all. The question is, can Lemonade deliver a better price for the long run? While Lemonade promotes $5 renters insurance, they’ve made a change to their site. Previously, the default personal property coverage started at $10k, which resulted in a $5 monthly renters insurance quote in NYC. Now, the default personal property coverage starts at $40k, which results in a $12.25 monthly renters insurance quote in NYC. This change may cause some confusion for those who are expecting lower prices, and I believe this is a move to help the company increase profits without increasing rates.

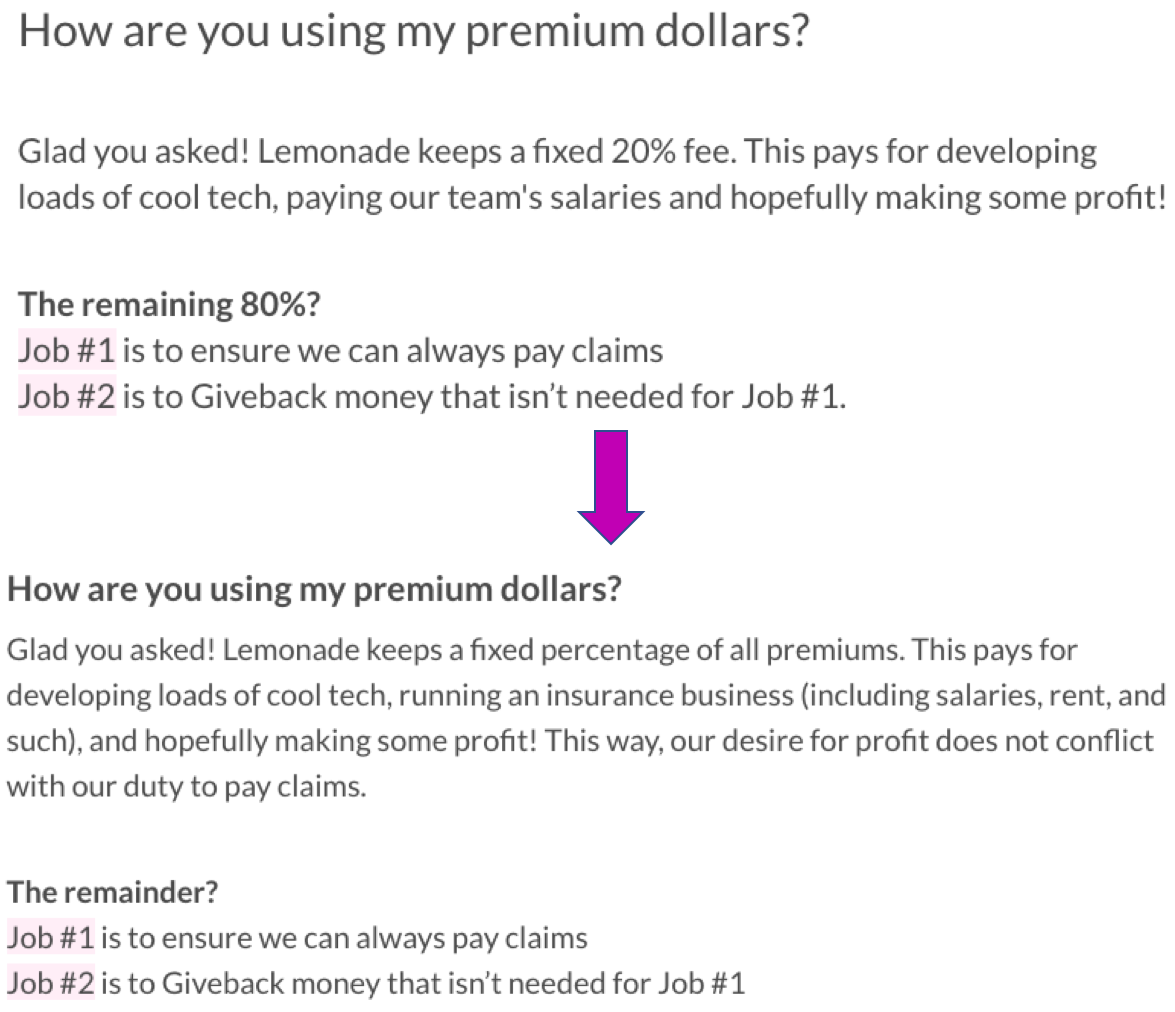

The Trust Card. “Insurance brands are some of the least loved and least trusted, and we came to understand that the cause is structural: every dollar your insurer pays you is a dollar less for their profits. Their interests, in other words, are profoundly conflicted with yours.” We’ve heard these words by Lemonade over and over again. And while Lemonade ‘solved’ this conflict by only taking a flat fee and giving unclaimed money to charity, are they really a conflict-free company? Do they not have a strong desire to improve their loss ratio? Isn’t the loss ratio an important part of their business? Will they be able to attract investors or potential buyers with a high loss ratio? And what about Lemonade’s reinsurance partners that paid $3.53 for every $1 in premium they received from Lemonade in the first quarter of 2018? “But the fact that our reinsurance agreements protect us from too many claims can’t hide the fact that, since launch, we’ve paid out more in claims than we’ve collected in premiums. Clearly, that can’t continue indefinitely.” Btw, transparency is one element Lemonade uses as part of the trust card and they are not being very transparent here (they went from a “20% fixed fee” to a “fixed percentage“):

The Data Card. “Being built from scratch on a digital substrate means we collect about 100X more data than traditional carriers. That’s why it won’t take us a hundred years to reach data-parity with incumbents. We guesstimate we’re 12-24 months away, and well-placed to outperform incumbents thereafter.” Lemonade is talking more and more about data, and while not being specific as it “goes to the very core of Lemonade’s IP,” ultimately, it will allow the company to “price risk at a far higher degree of resolution.” Let’s assume that Lemonade does have superior data than traditional insurers that will enable better underwriting – at the end of the day, it all depends on what they decide to do with it. You see, some ignore data that predicts risk, while others don’t.

If Lemonade goes by their data to “quantify risk like never before,” then they could become a boutique insurer by offering attractive prices to low-risk customers, while pricing-out high-risk ones. On the other hand, their temptation to grow may cause them to ignore some datasets and take on more risk.

Your Turn

Lemonade brought color to the insurance industry.

You know your industry is not boring when @aplusk feels compelled to weigh in on the latest #insurance incumbent vs. #insurtech startup spat! #EndOfInsurance https://t.co/TuMB5GAv6S

— Rob Galbraith (@robgalb) October 21, 2018

It also brought a bunch of copycats and it’s making several insurers get out of their way – Aviva is just one example. Last week, Northwestern Mutual announced the funding of four grants totaling $600k to support childhood cancer research – did you hear about it? I’m sure most of you haven’t. Lemonade didn’t invent social causes, trust, or data – they’re just very vocal about them. At the end of the day, Lemonade doesn’t have the right cards to win the insurance marathon, but that doesn’t mean they aren’t intimidating (and attracting) others by sprinting. So, focus on the right cards and don’t forget – insurance is not broken, just bent.