The Guardian Way

Back in December 2017, Gryphon Group Holdings , reached an agreement to acquire Guardian Assurance Limited and the rights to its trading names. The news followed an announcement by Daniel Pender – back then the CEO of Gryphon – announcing a £180m funding round from investors to design, build and launch an insurance challenger that seeks to protect more families in the UK. That was then. This is now.

From 1821 Into the 21st Century

Guardian, the heritage insurance brand founded in 1821 is being brought into the 21st century with a newly launched identity for their protection business with the promise of Life. Made Better.

“Our ambition is for every family to have protection that they truly believe in. For us, ‘better’ isn’t about changing one big thing; it’s about improving lots of little things across proposition, adviser experience and company culture that collectively make a big difference. ‘Better’ is our driving force. We’re working hard to create a company that brings our brand promise alive for both customers and advisers. We believe the rebirth of Guardian will have a positive impact on the market and ultimately, more families will be protected.” – the newish CEO of Gryphon, Simon Davis.

The company plans to focus on five key areas for challenging the typical way of doing things: (1) Products – making them clearer and easier to understand, (2) Liberating technology – without legacy systems in the way, the company will harness the power of technology to deliver an effortless digital experience, (3) Fairness – putting the protection needs of customers first, (4) Forward thinking underwriting – underwriting with the future in mind to meet the growing needs of customers, and (5) Customer care – claims support will be completely customer centric.

The Guardian Way

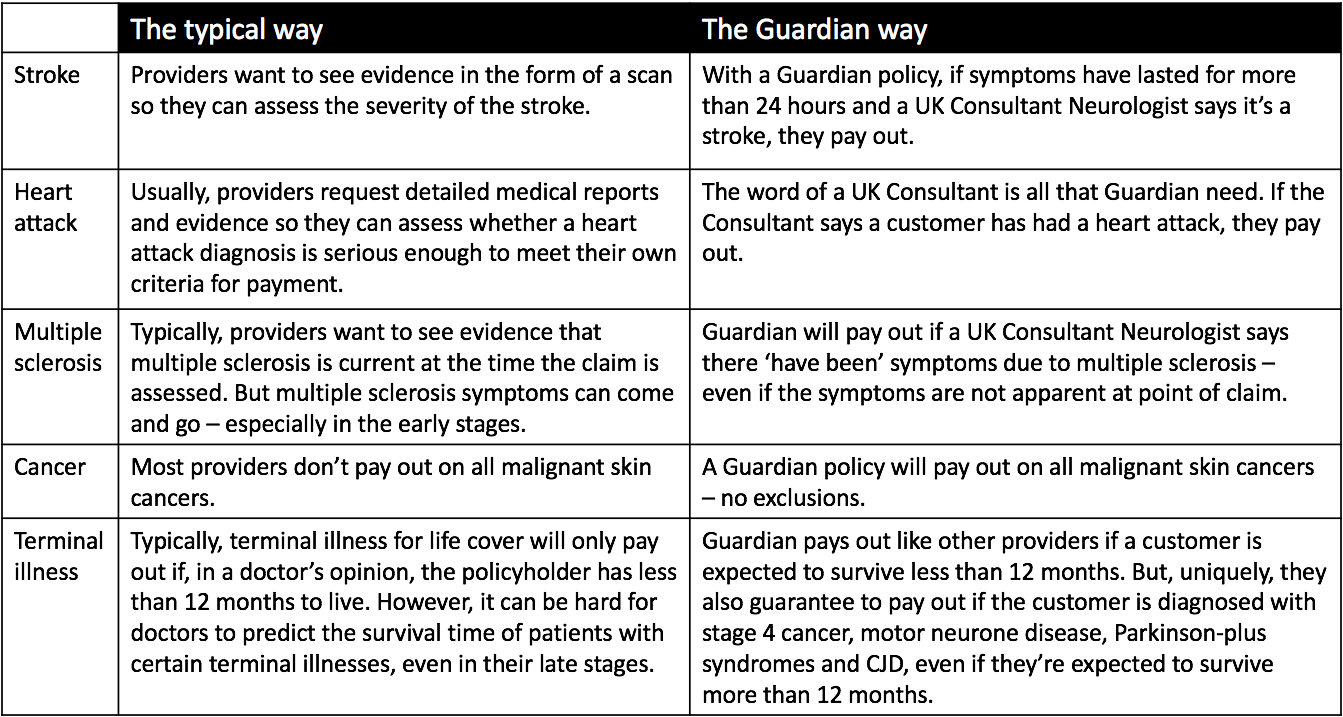

Guardian’s new life and critical illness product will have simpler, broader definitions with no general exclusions. Below is an example that demonstrates the difference between the old way and the Guardian way:

Also, Guardian will be distributing its products exclusively through advisers, using a technology platform called Protection Builder. The platform is based on individual covers which can be combined within one policy, with multi-life and multi-cover discounts. Features include: (1) single question set – automatic underwriting for the maximum amount of protection the company is prepared to offer across all types of core cover, (2) dual cover – different covers with different sums assured for different lives can be covered in individual policies within a single application, (3) multi-cover discount – discount for joint applicants (dual lives) or other multi-cover policies, (4) smart form – responds to an applicant’s answers by always asking the next logical question about any existing medical conditions, (5) optional extras – fracture cover and children’s CI are additional options, and (6) payout planner – nominating beneficiaries is built into the online process, which enables Guardian to pay the beneficiary without waiting for probate to be granted.

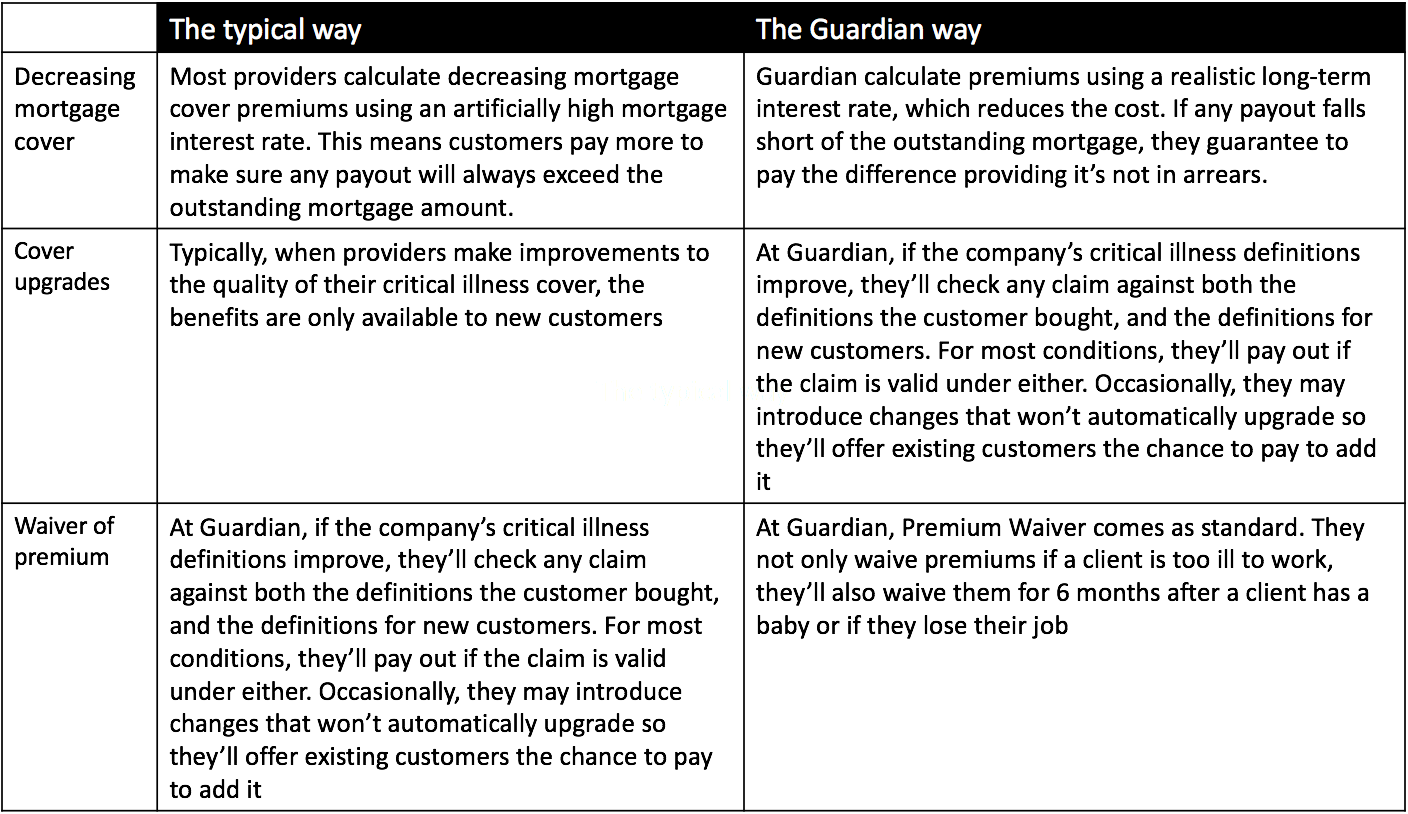

Guardian’s strategy is about being fair to customers, from interest rates used to set premium calculations for mortgage cover, to ways the company treats customers. Examples below:

Guardian is taking a more personal approach to claims support. In the event of a claim, the company does not have a set list of services to choose from. Instead, its introducing a service called HALO, which is about identifying each claimant’s specific need and delivering through the company’s network of medical, legal and financial experts.

“Our whole business is about helping customers through difficult times. When it comes to claims support, it needs to be personal. Whether it’s the little things like identifying what support is available after spending time in hospital, or the bigger things like estate planning following a terminal illness diagnosis, Guardian’s HALO service is designed to offer bespoke and valuable support.” – CEO of Gryphon, Simon Davis.

Guardian’s initial plan is to focus on life and critical illness, followed by income protection later. It is now in a pilot, phase, working with a few firms and expects to be widely available across the market by the end of the year.