Lemonade files for IPO

Lemonade announced it has filed for its initial public offering with the U.S. Securities and Exchange Commission. The company intends to list its shares on the New York Stock Exchange under the symbol “LMND”. The number of shares to be offered and the price range for the proposed offering have not yet been determined.

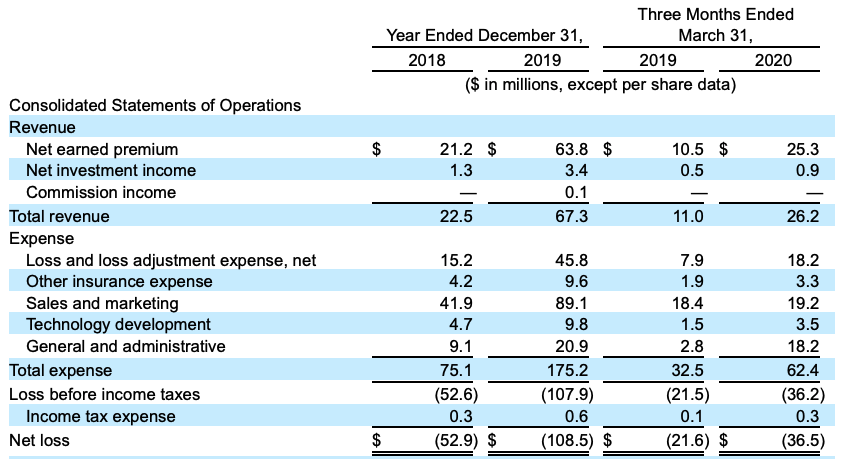

According to the S-1 filing, Lemonade has not been profitable since its inception in 2015 and had an accumulated deficit of $198.3 million and $234.8 million as of December 31, 2019 and March 31, 2020, respectively. The company incurred net losses of $52.9 million and $108.5 million in the years ended December 31, 2018 and December 31 2019, respectively, and a net loss of $36.5 million for the three months ended March 31, 2020.

Since launching in late 2016, Lemonade’s gross written premium grew from $9 million in 2017, to $47 million a year later, and to $116 million in 2019. For the three months ended March 31, 2020, GWP was $38 million. In parallel, net losses per dollar of GWP dropped from over $3 in 2017 to under $1 both in 2019 and for the three months ended March 31, 2020. Revenue was $2 million, $23 million, and $67 million in 2017, 2018 and 2019, respectively, and net losses were $28 million, $53 million, and $109 million, respectively. For the three months ended March 31, 2020, revenue was $26 million and net losses were $37 million.

The company’s sales and marketing expenses increased $47.2 million, or 113%, to $89.1 million for the year ended December 31, 2019 compared to the year ended December 31, 2018. The expense related to brand and performance advertising, the largest component of its sales and marketing expenses, increased by $39.8 million, or 110%, in 2019 as compared to 2018, as a result of increased spending on search advertising and other customer acquisition channels.

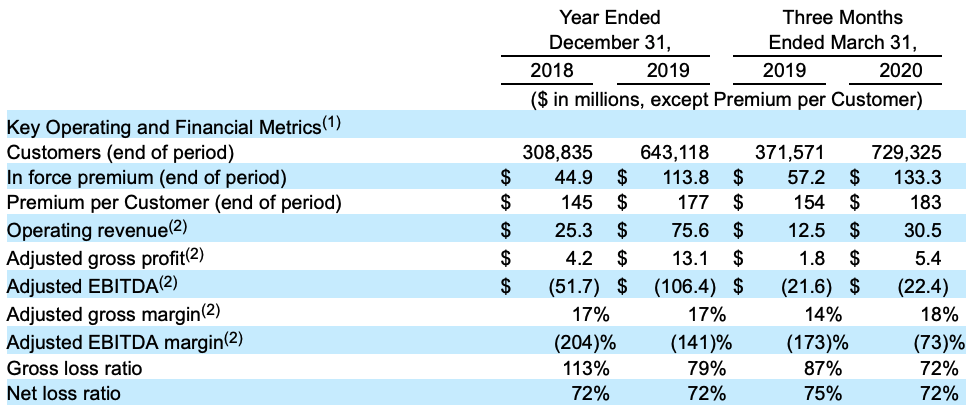

Lemonade has seen “significant improvement” in their marketing efficiency, which they evaluate by comparing the growth of in-force premiums to marketing expenditures for a given period. For example, since March 31, 2019, marketing efficiency roughly doubled, such that Lemonade is currently able to acquire more than $2 of in-force premium for each $1 of marketing investment. Lemonade believes that by applying a roughly 20% gross margin, it would earn back the cost of acquiring customers in just over two years, and any annual coverage increases, graduation of renters to homeowners or new product introductions, pet insurance for example, further shorten the payback period and drive up lifetime value.

Approximately 70% of Lemonade’s current customers are under the age of 35, and about 90% of customers said they were not switching from another carrier.

As of March 31, 2020, the median age of a Lemonade customer with an entry level $60 a year policy – corresponding to $10,000 of possessions – is about 30 years old. This climbs towards 40 for customers with policies of about $600, and among the handful of customers paying approximately $6,000 a year, the median age is about 50.

As of March 31, 2020, Lemonade had 12,445 customers of condo insurance policies, 10% of whom had graduated from the company’s renters policy.

The average renter pays Lemonade nearly $150 per year, and that jumps to around $900 for owners of homes and condos.

In regards to Lemonade’s business model, the company states that it typically retains a fixed fee, currently 25% of all premiums. The remaining funds to pay claims (including reinsurance) and, if there are funds left over, donate to nonprofits as part of the company’s giveback program, which has supported nonprofits with over $800,000 so far.

Beginning on July 1, 2020, Lemonade will have proportional reinsurance protecting 75% of the business. Under the Proportional Reinsurance Contracts, which spans all of the company’s products and geographies, Lemonade will cede 75% of premiums to their reinsurers. In exchange, reinsurers pay Lemonade a ceding commission of 25% for every dollar ceded, in addition to funding all of the corresponding claims, i.e. 75% of all claims.

Goldman Sachs & Co. LLC, Morgan Stanley & Co. LLC and Allen & Company LLC are acting as the managing bookrunners for the proposed offering. Barclays Capital Inc. is acting as a bookrunner. JMP Securities LLC, Oppenheimer & Co. Inc., William Blair & Company, L.L.C. and LionTree Advisors LLC are acting as co-managers for the proposed offering.