Economical Insurance Reports Financial Results for First Quarter 2017

Highlights

– Acquired the market leader in the Canadian pet insurance industry, which it renamed Petline

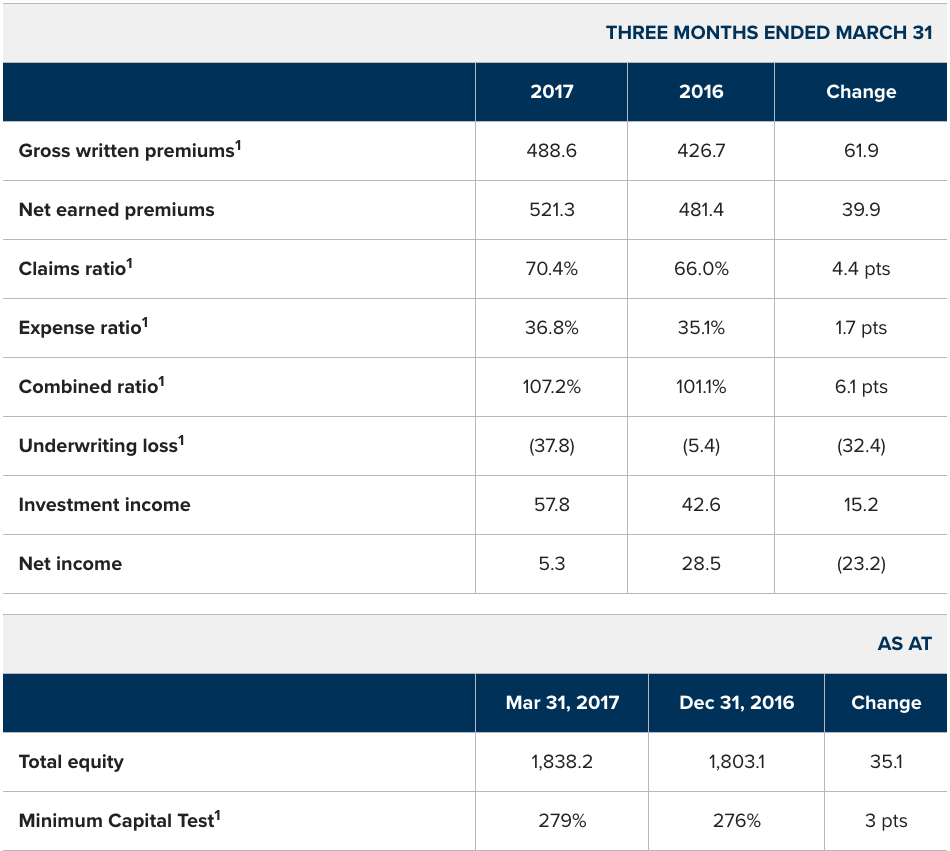

– Increased gross written premiums by 14.5% over first quarter 2016, driven by strong personal lines growth, including contributions from Sonnet and Petline

– Reported a combined ratio of 107.2% for the quarter, including an impact of 6.5 percentage points related to Sonnet and the replacement of our personal lines policy administration system

– Generated net income of $5.3 million for the quarter

– Increased total equity by $35.1 million since December 31, 2016 to $1.8 billion

Economical Insurance, one of Canada’s leading property and casualty insurance companies, today announced consolidated financial results for the three months ended March 31, 2017.

“We are pleased to welcome Petline to the Economical family and are excited by the opportunities for this new line of business,” said Rowan Saunders, President and CEO. “However, we continued to be challenged by the performance of our auto lines, and were impacted by increased levels of catastrophe losses and relatively worse winter weather conditions. Ongoing investments in Sonnet and the replacement of our personal lines policy administration system also contributed to the increase in the combined ratio. A number of measures including improvements in pricing, underwriting, and claims actions are being implemented, but will take time to be reflected in our results.”

Recall definition of combined ration.

Gross written premiums for the first quarter of 2017 grew by $61.9 million or 14.5% over the same quarter a year ago from a combination of organic and inorganic growth. Personal lines premiums grew by $53.3 million or 20.5% primarily due to increased auto policy volumes in our broker channel, our digital direct distribution channel, Sonnet, and the acquisition of Petline. Commercial lines premiums grew by $8.6 million or 5.2% driven by targeted rate increases for commercial property and liability, and increased fleet business.1These items are non-GAAP measures which are defined below. Claims ratio, expense ratio, combined ratio, and underwriting loss exclude the impact of discounting.

Underwriting activity for the first quarter of 2017 produced a loss of $37.8 million, resulting in a combined ratio of 107.2%, compared to an underwriting loss of $5.4 million and a combined ratio of 101.1% in the same quarter a year ago. Underwriting results were impacted by continued challenging auto performance, mainly in Ontario, British Columbia, and Alberta. The quarter was also impacted by $7.7 million of net catastrophe losses, compared to none in the same quarter a year ago. The first quarter saw relatively worse winter weather conditions compared to a benign first quarter of 2016. We continue to make significant investments in Sonnet and the replacement of our personal lines policy administration system, which impacted the combined ratio by 6.5 percentage points, compared to 2.5 percentage points in the same quarter a year ago. We expect that these strategic investments will continue to increase operating expenses during the implementation and start-up phases, but are expected to improve our operational efficiency and profitable growth in the longer term.

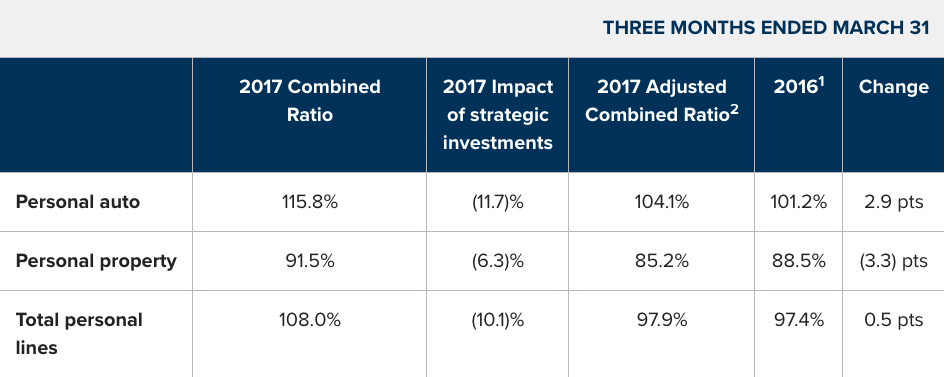

Line of Business Combined Ratios

In 2017, the results of the underwriting activity of Sonnet have been included in the line of business performance resulting in increased combined ratios, which will continue during the start-up phase. In addition, our investment in a new personal lines policy administration system has further increased the combined ratios. The collective impact of these strategic investments on the 2017 combined ratios has been noted in the table below to depict the adjusted combined ratios excluding these investments for comparative purposes.

Personal insurance

1 In 2016, the personal lines of business results excluded certain expenses associated with the development and launch of Sonnet as it was in the pre-launch phase for the majority of the year.

2 This item in a non-GAAP measure which is defined below.

The adjusted personal auto combined ratio for the first quarter increased due to continued profitability challenges mainly in Ontario, British Columbia, and Alberta. Despite reforms to Ontario auto insurance, many insurers have recently filed or implemented rate increases to address rate deficiencies in this line of business. To address these challenges we are implementing a number of measures including improvements in pricing, underwriting, and claims actions. However, these measures will take time to be reflected in our results.

The adjusted personal property combined ratio continues to be strong and now includes the results of Petline. Increased catastrophe losses in this line of business were largely offset by a decrease in large losses. Overall, on an adjusted basis, personal lines produced underwriting income of $6.9 million compared to underwriting income of $7.9 million in the same quarter a year ago.

Commercial insurance

The commercial auto combined ratio was impacted by an increase in claims frequency compared to the first quarter of 2016, which benefited from unusually low frequency primarily due to benign weather conditions. Pricing improvements are being implemented, and we are reviewing this line of business to determine if additional actions are required.

The commercial property and liability combined ratio was relatively unchanged. Decreases in favorable claims development and increased catastrophe losses were largely offset by a decrease in large losses, a decrease in the expense ratio, and the beneficial impact of increased rate resulting from our underwriting and pricing actions. Previous actions have stabilized this book of business and we continue to develop our plans for future profitable growth. Overall, commercial lines produced an underwriting loss of $10.8 million compared to an underwriting loss of $1.8 million in the same quarter a year ago, primarily due to the deterioration in commercial auto underwriting performance.

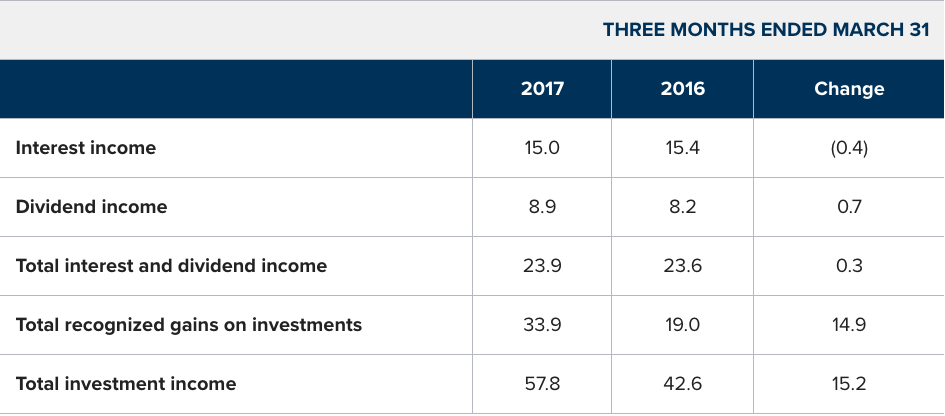

Investment income

Recurring investment income was relatively stable during the first quarter of 2017, compared to the same quarter a year ago, as the decline in interest income was more than offset by an increase in dividend income. Recognized gains increased significantly due to strong performance by global equities, increased sales of domestic equities, and higher bond valuations arising from a decline in yields.

Net income decreased by $23.2 million over the same quarter a year ago as higher investment income was more than offset by higher underwriting losses driven largely by increased spend on our strategic initiatives, as well as continued challenges in auto performance, relatively worse winter weather conditions, and increased catastrophe losses.

Economical’s capital position remains strong. Total equity exceeded $1.8 billion at March 31, 2017, an increase of $35.1 million or 1.9% since December 31, 2016, primarily due to market value increases within the investment portfolio. Economical’s minimum capital test ratio is at 279%, which remains significantly in excess of both internal capital management and external regulatory requirements as of March 31, 2017.

Bottom Line: 1. Engaged in M&A. 2. Proud of its digital brand Sonnet. 3. Challenged by auto. 4. Doing away with legacy systems. 5. And always ‘improving pricing’.