An 84-year reign came to an end, and more

May 2026 was a month of endings. An 84-year reign. A California market that keeps getting smaller. A workforce reduction attributed, plainly, to AI.

The throne changed hands.

S&P Global Market Intelligence estimated that Progressive has overtaken State Farm as the largest U.S. private passenger auto insurer. State Farm had held that position since 1942. It did not lose it in a single quarter — it lost it over several years of underwriting discipline problems, rate inadequacy, and a prolonged effort to stop the bleeding.

State Farm’s own Q1 2026 results confirmed a different turnaround: its P&C carriers swung from a $5.1 billion underwriting loss a year ago to a $1.8 billion gain, with auto going from -$3.6 billion to +$1 billion. Written premiums rose 1.9% to $27.9 billion.

Progressive, meanwhile, posted a 90.2% combined ratio for April, reported $1.1 billion in net income for the month, expanded its Snapshot telematics model to 14 states, and spent a record $1.5 billion on advertising in Q1 — up 20% year over year. The gap between the two companies right now is not about size. It is about momentum.

California kept shrinking.

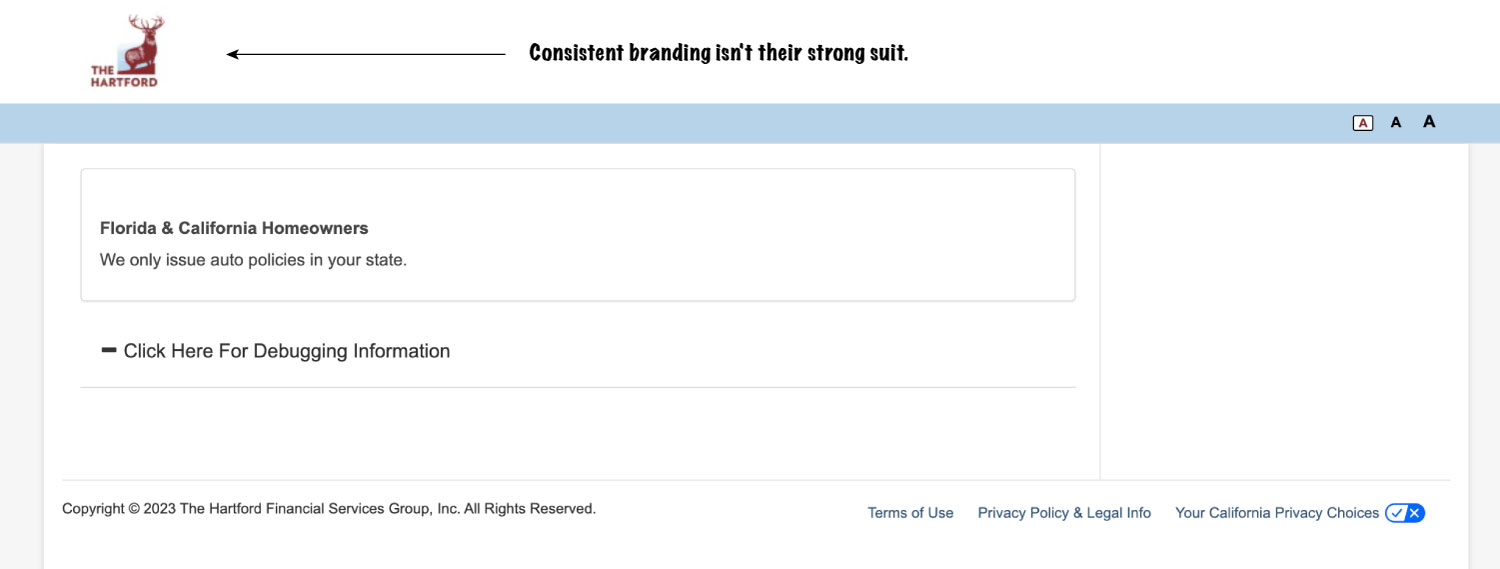

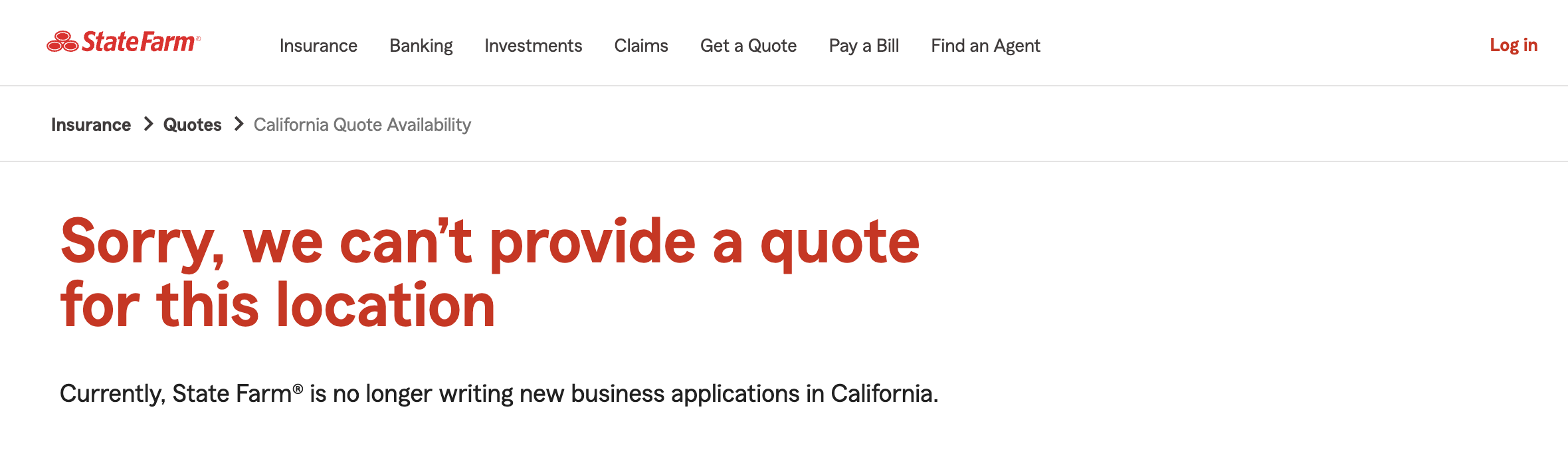

Hartford announced it will no longer sell new homeowners policies in California, joining a list that keeps getting longer. State Farm, which is still contending with a lawsuit from California’s attorney general over its wildfire claims handling, stopped writing new business in the state in 2023. The regulatory environment, reinsurance costs, and loss exposure have made the math increasingly difficult to justify. Hartford framed its exit as a response to the market’s “unique challenges.”

Farmers, notably, moved in the other direction — receiving California Department of Insurance approval for a new homeowners rating plan tied to Commissioner Ricardo Lara’s Sustainable Insurance Strategy.

“Farmers is proud to be one of the few home insurers that never stopped offering new home policies in the state and we remain committed to the California marketplace. It’s also important to note that we have been able to stay in the market and continue to serve our customers because key stakeholders, including the California Department of Insurance, have remained steadfast in working toward meaningful solutions to reinvigorate the state’s insurance marketplace.”

The big are getting bigger, but…

Berkshire Hathaway agreed to acquire homebuilder Taylor Morrison for $6.8 billion, a move that extends the conglomerate’s exposure to the U.S. housing market and signals Greg Abel’s willingness to make large bets even as he flagged increasingly competitive insurance conditions. Abel’s comments at the annual meeting (3:44 minutes into the video) — that conditions in the insurance market are becoming less favorable — were worth noting alongside GEICO’s Q1 results, which showed a $1.4 billion underwriting profit, a 34% decline from the same period last year.

Intact Financial was reported to be exploring a potential acquisition of Hiscox, which sent Hiscox shares sharply higher.

AI moved from strategy decks into org charts.

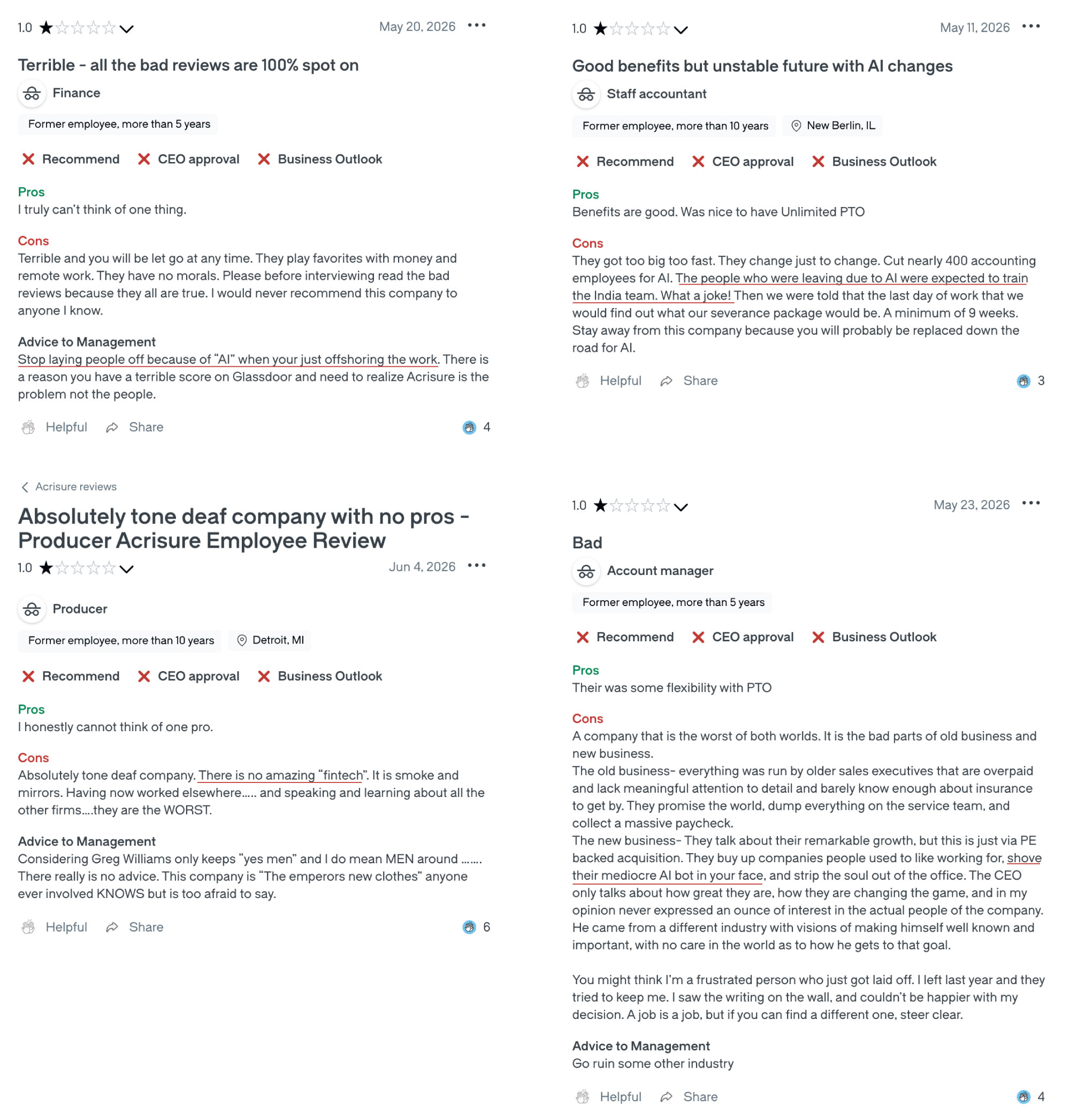

Acrisure announced it is laying off approximately 2,250 employees — about 11% of its workforce — and cited advances in AI, technology, and digital platforms as the reason. The layoffs will continue through 2027.

Acrisure is not alone in the direction, just the most explicit. Brown & Brown said AI will automate 25% of submission workflows. Aon expanded its Claims Copilot globally. Liberty Mutual launched a conversational AI quoting app inside ChatGPT — the first carrier-backed integration of its kind — initially in seven states with plans to reach more than 40 by year-end.

Pinnacol Assurance cut 43 positions, about 7.5% of its workforce, describing it as a proactive restructuring.

One case worth remembering.

Pennsylvania’s attorney general reached an agreement with GEICO requiring changes to its AI-assisted underwriting review process after an investigation found a customer was unknowingly left uninsured following an AI-driven cancellation. It is the first state-level regulatory intervention directly targeting an insurer’s AI underwriting system. It will not be the last.