allai launching insurance AI app store

Canadian insur-tech startup allai is taking an innovative approach to AI for the Canadian insurance industry. A Q&A with allai founder Carlos Benfeito .

What is an AI “app store”?

There are 2 types of “friction” we are tackling at allai. First of course is insurance friction and second is AI friction.

Many of the existing options on the market are based on an “AI as a Service” model where the customer, policy, claims data must “live” in a provider’s cloud or data center. This causes concern with regards to not only privacy and security for the insurance industry but also adds friction over data intellectual property (IP). It’s a pretty big obstacle right now and it’s increasingly becoming a barrier.

So, if you think of an app and an app store, you choose the capability you want, say a restaurant app, and download it and run it on your phone. We are taking the same approach at allai but instead of apps these are aims. The broker or carrier can select, download, deploy aims in their data center or on their cloud, we never see or have access to their data IP. They can then use the aim AI capabilities as part of their own solutions.

Ok let’s back it up a bit and tell us a little about allai

allai creates AI capabilities for the Canadian insurance industry, helping insurers simplify, brokers delight, Canadians demystify, insurance. If you consider the digital NPS scores for the insurance industry across purchasing, modification, claims and renewal there is a lot of room for improvement there.

We are launching a set of aims (those are the “app like things”) that are focused on helping in those areas, across personal lines auto, personal lines property and later on in commercial lines.

Each of our aims is focused with helping the top line, bottom line, as well as giving brokers, carriers or vendors insights into customer behavior, customer interests, strengthen the relationship and delight the customer.

Can you provide a concrete example of an “aim”

A concrete example is our auto lenz aim. If we start with the most basic aspect of the auto lenz aim, it allows an existing insured or a potential customer to take a photo of a car and the auto lenz aim infers the make, model and year variables for the vehicle. There are a couple of options on the market that offer a similar base capability, blippar is one such example.

The auto lenz aim goes a couple of steps further. It provides a bunch of Canadian data around safety rankings, fuel consumption, claims index, recalls etc. that the broker and carrier can in turn use and provide to the customer. If you think about that for a second, how many different websites or apps would the customer have to visit to get all of that information at the same time as getting a quick quote or doing a what if scenario ? We also have some fun data sets like “is that car famous” that provides the list of movies that the specific car make and model have appeared in, all at the snap of a pic.

The auto lenz aim also generates customer insights for the broker or carrier. For example, what types of vehicles is the customer considering ? Where is the customer shopping for cars, dealerships ? Was the customer attending any events, car shows ? The auto lenz aim will also perform image analysis to see what other products may be of interest for the customer. Are there bicycles, motorcycles, boats etc. in the photo’s ?

The broker and carrier can offer this during purchasing, providing a simple and fun path to a quick quote or offer quick what if scenarios for existing customers, a “know your vehicle” feature or as a way for the customer to check back in with the brokers or carrier’s app for recalls etc.

When you consider that there are 3 million used vehicles and 2 million new vehicles sold in Canada per year with 22 million registered vehicles, combine the fact that there were 105 billion photos taken, 80% of which were on mobile devices (referencing US stats), it becomes a very interesting user experience proposition.

For the broker and carrier this is a way of putting them at the forefront of the shopping experience instead of just at the moment of truth, helping build that relationship and providing a feature that helps them move to a role of a trusted adviser.

How many of these aims will be in the allai store?

There are many areas where the AI fields of computer vision and natural language can be applied to help brokers and carriers tackle the various insurance friction points when you look across the life cycle of an insurance policy, especially as consumers move towards natural user interfaces and natural user interactions.

Our “app style” approach with aims means that we offer these micro AI capabilities where brokers and carriers can pick and choose what they want to use and how they want to apply AI in their processes and customer experiences. When you add to that that each line of business requires its own set of aims, let’s just say that there is enough to keep us and the industry busy for a little while.

At the end of the day we offer the aims that Canadian brokers and carriers need to keep up with the “disruptors”, enable them to make their own lemonade so to speak.

So allai is an enabler, correct?

We see ourselves as both an enabler and a disruptor. We are enablers in the sense that we are not selling insurance products like say Lemonade, Metromile, Trov etc. We offer the capabilities that these great startups are using to disrupt the incumbents and make them available to the Canadian insurance industry. In that sense yes, we are definitely enablers.

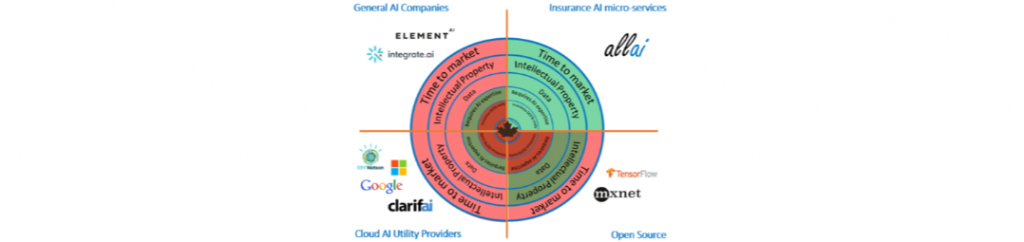

We are more of a “disruptor” for the “AI as a Service” model. For example, if you take the tech giants in this space like Microsoft, Google, Amazon, IBM etc. they offer these incredible but “generic” AI capabilities, generic in that their API’s do not understand insurance out of the box, in particular Canadian insurance, and with each of those offerings the brokers or carriers data ends up in someone else’s cloud.

If you look at some of the other exciting options like clarifai, api.ai or wit.ai, again same AI friction points, data IP, not out of the box ready for Canadian insurance etc. We have these incredible Canadian AI companies like Element AI and others, that are also taking this AI as Service approach, but again the same AI friction points for the Canadian insurance industry are emerging.

With the aim approach we are taking at allai, where like an app in an app store you select, download, deploy and use the ready for Canadian insurance AI capabilities you need, the broker or carrier has total exclusivity and control over their IP, their data, it’s the opposite of what the AI as a Service providers are offering. In that sense I would say we are disrupting the AI operational model that we are seeing applied in a rinse & repeat pattern .

What makes it “Canadian AI” eh?

It’s important for us to deliver on the “ready to use insurance AI” promise. To do that we need to take many factors into consideration, one of which is localization, this impacts insurance AI in various ways. Having said that our approach and technology is being engineered without borders.

If we go back to the auto lenz aim covered earlier, there are vehicles only sold in Canada that we need to take into consideration, for instance the Chevrolet Orlando, no longer manufactured now but it was sold in Canada and not the US, so we need to take those types of things into consideration when training the AI. This applies to all of the data sets that come with the auto lenz aim. The recall data, the location analysis, the fuel consumption data, it all needs to be engineered and the AI trained for the Canadian insurance industry.

This obviously becomes extremely important when it comes to training the AI around insurance coverage’s, insurance language, insurance risks, insurance regulation etc. These all need to be done in context of the Canadian insurance industry.

Another important part that makes the allai aims ready for Canadian insurance is that we will base all of our API’s, the data model we use to train our AI, how the aims integrate with broker or carrier systems, on the CSIO standard. There are some challenges with that, but it is an important part of what makes insurance AI capabilities … Canadian AI insurance capabilities.

For the US market our aims would be localized in part by using the ACORD standard instead of CSIO.

When can Canadian brokers and insurers start using aims?

All the aims released in the aim store will be available to download for free so that brokers and insurers can try them out, we want to remove the friction and walk the walk. We are excited about that.

With that said we are targeting July 2018, we are really looking forward to that. We will have a few of the aims ready for launch with more being released as they are ready. In the meantime, brokers and carriers can have a look at what we are working on at allai by exploring the aim store.

What about brokers and carriers that are taking on AI themselves?

A couple of points on that. Our approach means that each of the aims is an AI specialized in handling a piece of an entire puzzle, in that context if a broker or carrier decides that they are going to build their own or use another option for certain AI capabilities they can still fill in the missing pieces using only the aims that make sense for them. It’s not an all or nothing approach. Coming back to the concept of the app store, I don’t download the entire app store catalog if I only need a restaurant app and we want to enable that same type of choice and agility through the aim approach.

Second thing I think we will start to see is that the limits to DIY will become apparent very quickly due to cost. For example, dealing with natural user interfaces (NUI’s) as opposed to graphical user interfaces (GUI’s), in a GUI world, a web page or a screen in an app, you have a very finite number of possibilities that you need to take into consideration. If you only have 10 questions on your screen than that’s all you have to deal with. Each question is known before hand, the responses are very controlled with drop down lists, check boxes, radio buttons etc. It’s a very controlled and manageable interface that DIY’ers can build and make beautiful.

When you get into the world of NUI’s it’s a different challenge. The amount of variations that you need to deal with, the contexts that need to be taken into consideration, just answering a question like “what is my policy number” through natural language, what policy, your auto policy or your property policy ? Did the customer use the word policy or contract or insurance number etc. Each of these needs to be handled by the AI to have a great user experience. This requires many hours of training the AI with the right types of data sets. There are various great open source frameworks that offer generic NLP capabilities but none of them can handle what is my policy number out of the box. If you take a birds-eye view to the insurance industry that would require many companies investing in inventing/reinventing the wheel.

As we start to release our portfolio of insurance aims around computer vision and natural language we want to provide brokers, carriers and vendors the most complete set of insurance AI capabilities in the industry to enable them to help their customers using the simplest and most natural interface possible.

Finally how do you pronounce allai?

🙂 like the word “ally”.