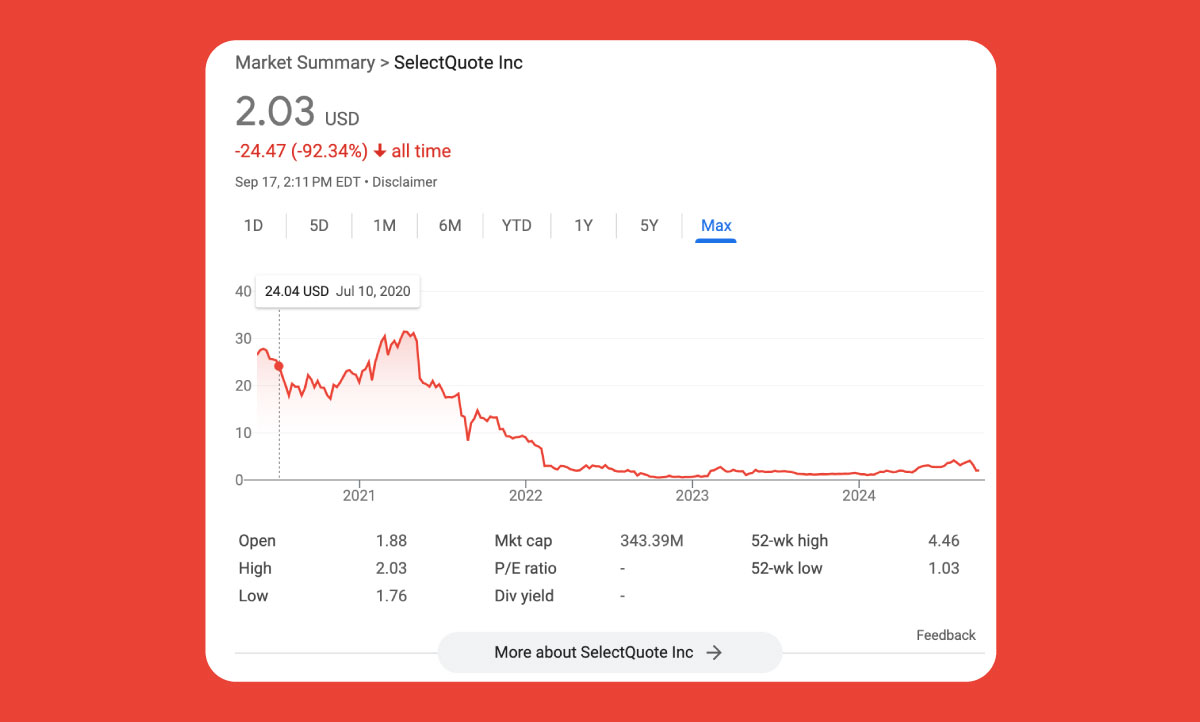

SelectQuote’s Q4 2024: Revenue soars 39%, but growth faces new challenges in 2025

SelectQuote Insurance Services shared its Q4 2024 financial results on September 13, led by CEO Tim Danker. Below are the key highlights:

- Financial Performance: SelectQuote reported Q4 2024 revenue of $307.2 million, a 39% increase from Q4 2023. Despite the growth in revenue, the company posted a net loss of $31 million, a 35% improvement from the $47.8 million loss in Q4 2023. Adjusted EBITDA for Q4 2024 was $14.4 million, compared to a loss of $5.8 million in the same quarter last year. For the full fiscal year 2024, revenue rose to $1.3 billion, while the net loss improved to $34.1 million from $58.5 million in FY 2023.

- Fiscal 2025 Guidance: The company forecasts revenue between $1.4 billion and $1.5 billion and adjusted EBITDA of $90 million to $120 million for fiscal 2025. The guidance reflects a cautious approach as the company focuses on profitability over growth in the coming year.

- Strategic Moves and Capital Structure: SelectQuote signed a nonbinding letter of intent with term lenders to securitize around $100 million. If completed, this deal would help improve the company’s capital structure by extending its term debt maturity to the fall of 2027, providing more time to achieve its long-term goals. CEO Tim Danker emphasized that while SelectQuote has ample liquidity, growth in 2025 will be more measured as the company prioritizes financial stability and profitability.

- Segment Performance:

- Senior Segment: Medicare Advantage (MA) policies grew by 8% in fiscal 2024, outperforming the initial forecast of a 10% to 15% decline. This growth was driven by improved efficiency and strong policyholder retention, resulting in a 25% EBITDA margin, slightly down from 26% in 2023.

- Healthcare Services: This segment showed robust growth, with membership increasing by 68% year-over-year to 82,000, significantly above the projected 25% growth. Revenue in Healthcare Services grew by 75% to $145.2 million.

- Life Insurance: Q4 2024 revenue was $42 million, up 11% year-over-year, with full-year revenue reaching $158 million, an 8% increase. The segment generated $7 million in EBITDA for the quarter and $20 million for the year.

- Auto & Home: The division contributed $8 million in Q4 revenue and $36 million for the year, with adjusted EBITDA of $2 million for Q4 and $14 million for the year. However, SelectQuote is scaling back this business by reducing agent headcount and lead sourcing to focus on more cash-efficient areas. As a result, Auto & Home will no longer be reported separately in future earnings.

- Strategic Shift: Moving forward, SelectQuote plans to maintain a small presence in Auto & Home, but it will no longer significantly contribute to earnings. This strategic shift is expected to negatively impact adjusted EBITDA in fiscal 2025 but will benefit overall operating cash flow for the year.

Bottom Line: “SelectQuote is still not as strong as we believe it can be. To be clear, SelectQuote has ample liquidity. But in 2025, our growth will be tempered for two reasons,” said Tim Danker. The two reasons are the later-than-expected timing of their initial securitization, which affects their ability to enhance the capital structure, and a change in commission structure with a major carrier partner that shifted from a more front-loaded to a back-loaded model for the upcoming Medicare Advantage season, impacting cash flows and limiting their capacity to hire more agents, thereby constraining growth potential.