Unhealthy Relationships

In business, there are order makers and there are order takers. An order maker controls the product/service, price, and quantity, while the order taker needs to adjust accordingly. Last week, Tesla, an order maker, cut the price of its vehicles by as much as 20%, forcing used car retailer Vroom, an order taker, to make an adjustment.

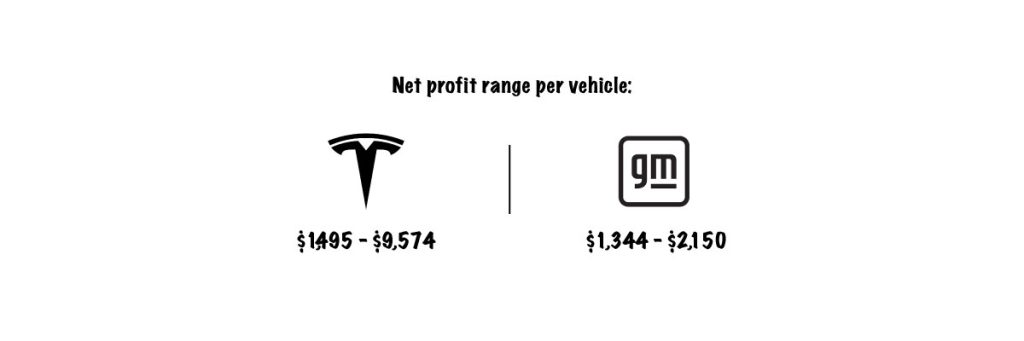

For some order makers, adjusting price is simpler than adjusting quantity. That’s the case with Tesla which leads the way in terms of vehicle profitability, according to a Reuters analysis.

When you’re an order taker, the nature of your relationship with order makers is important. In Vroom’s case, Tesla vehicles account for a small percentage of its inventory. Switching gears, some order takers in insurance have an unhealthy relationship with order makers.

This week, we covered the layoffs at Insurify, an order taker that is now scrambling as it tries to adjust to a future that may never be as good as the past. To understand Insurify’s struggles, let’s look at MediaAlpha, the bridge between order makers and order takers.

MediaAlpha, which is also an order taker, has seen its Q3 2022 revenue decline 42% year over year. This was driven primarily by a 53% decline in the company’s P&C vertical, which has historically accounted for over half of its revenue. MediaAlpha explained some of the reasons for this decline in a shareholder letter. The obvious one, which we’ve heard from other players such as EverQuote, is that carriers are concerned about profitability so they’re pulling back or limiting ad spend. Now, if you’re an investor in MediaAlpha, then you’ve been reassured that eventually, carriers will resume their normal ad spend. However, the other reason shared by MediaAlpha may not get better with time – a higher mix of transactions took place on its private marketplace. “This was driven by a larger share of transactions on our platform coming from our largest P&C demand partner, which utilizes our Private Marketplace option more extensively than average,” the company wrote.

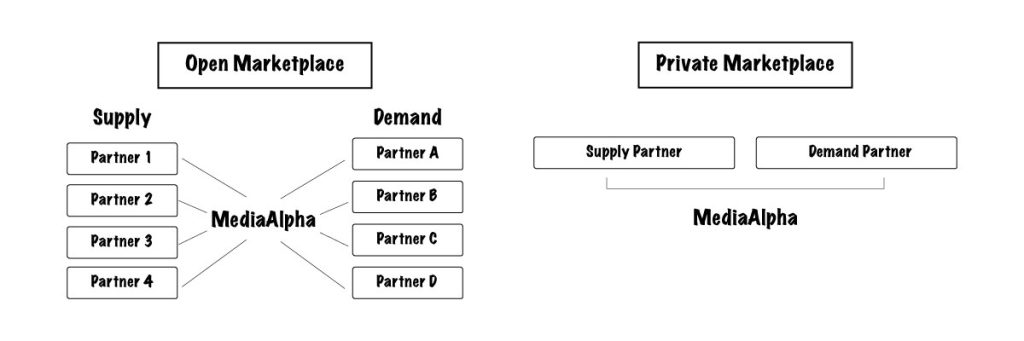

Before we move forward, we need to understand the terms used by MediaAlpha.

The company has two business models – the open platform model and the private platform model. In the open model, MediaAlpha has separate agreements with demand partners (generally insurance carriers and distributors) and suppliers, and it controls consumer referrals that are sold to demand partners. In the private model, demand partners and suppliers contract with one another directly, and MediaAlpha charges a platform fee from the demand and supply partners based on the consumer referrals transacted. The open model gives MediaAlpha more control, allowing it to make more money, but with the private model the company mainly acts as the bridge that connects two parties.

In a recent investor presentation, MediaAlpha described the open model as its core business.

Judging by past financial results, open platform transactions were indeed MediaAlpha’s core business. Below are some figures shared in the company’s S-1.

| $ in thousands | 6 months ended Jun 30, 2020 | 6 months ended Jun 30, 2019 | Year ended Dec 31, 2019 | Year ended Dec 31, 2018 |

| Open platform transactions | $237,984 | $167,845 | $399,945 | $291,331 |

| % of total transactions value | 69.7% | 70% | 71.4% | 73.3% |

| Private platform transactions | 103,271 | 71,839 | 160,180 | 105,924 |

| % of total transactions value | 30.3% | 30% | 28.6% | 26.7% |

| Total transaction value | $341,255 | $239,684 | $560,126 | $397,255 |

However, the share (percentage) of open platform transactions has decreased over the past few years, while the share of private platform transactions has increased.

| $ in thousands | 9 months ended Sep 30, 2022 | 9 months ended Sep 30, 2021 |

| Open platform transactions | $324,008 | $469,670 |

| % of total transactions value | 57% | 60.7% |

| Private platform transactions | 244,592 | 304,410 |

| % of total transactions value | 43% | 39.3% |

| Total transaction value | $568,600 | $774,080 |

When the pandemic hit and companies were forced to work remotely, some folks said it was just a matter of time before all employees returned to the office five days a week.

That did not happen.

With profitability concerns, some (like MediaAlpha) are saying that it is just a matter of time before carriers go back to their historical ad spend.

That will happen, but perhaps not in the same manner.

As some carriers (order makers) changed their customer acquisition strategies, order takers such as MediaAlpha, The Zebra, and Insurify had to adjust. Between January 2021 and January 2022, MediaAlpha increased its headcount by 23%, but there was no growth between 2022 and 2023. The Zebra and Insurify have gone through several rounds of layoffs. These companies are currently making quantity changes (reducing headcount) to adjust to the lower demand from carriers, but what if demand picks up in a different way?

In the good old days, Progressive paid some order takers a high double-digital figure for a consumer referral. What if that never comes back? A company like Insurify can withstand a period of lower demand, but transitioning to a situation where carriers aren’t ready to spend as much as they used to is a different ballgame that won’t be won by cutting costs.

In its shareholder letter, MediaAlpha attributed the higher private model transactions to just one demand partner. In EverQuote’s Q3 2022 earnings call, the company mentioned the financial impact caused by a single carrier. The Zebra relies heavily on Progressive, and Insurify’s revenue comes from a small number of partners – these are all unhealthy relationships and the future of these companies may be decided by a select few.