Tackling SME underinsurance with AI

With 50% of SMEs underinsured, many businesses are vulnerable if they suffer a loss. What can insurers do to help buyers find and purchase the right cover?

Around half of SMEs are underinsured

Underinsurance – inadequate insurance coverage held by a policyholder – is a problem for commercial insurers and policyholders alike.

With more than one-quarter of UK SMEs reporting they would go out of business if faced with an unexpected bill of £50,000, underinsurance represents a risk to the existence of many small businesses.

Based on reports from a variety of sources (including BCIS, CILA, FCA and major insurers) around one-half of UK businesses are underinsured, across multiple covers, to an average of 50% below the amount required to cover the loss. This translates to around £1bn of premium going uncollected in the UK SME market alone.

Why are SMEs persistently underinsured?

We see several reasons why underinsurance persists among SMEs:

1. Failure to purchase adequate cover

Inadequate cover is usually a result of misjudgment, either of the amount insured or the cover required. Although the majority of business owners are confident about their businesses’ insurance requirements, many of these SME buyers are in fact unknowingly underinsured.

There is a knowledge gap between business owners and insurers when it comes to selecting adequate cover.

SME cover also varies substantially across lines of business, with a substantial gap between the risks businesses say they face and the cover they hold. For example, just 16% of SMEs have cyber insurance, despite an additional 46% recognising that its relevance to their business.

2. Unawareness of specialist cover

SMEs can often be unaware of the existence of relevant specialist covers, such as cyber risks or directors and officers liability insurance.

In our last post we sought business insurance quotes for a virtual business, from several leading online business insurance platforms. Not all these platforms offered cyber risks cover for our fictional software engineering house. An SME buyer purchasing direct may not realise when they are not being offered a comprehensive range of covers.

3. Failure to update cover as needs change

Businesses, particularly small ones, are fast changing entities. If a business grows fast – opening new premises, or holding an increased quantity of stock – then its insurance needs will change rapidly within a single 12-month policy.

In addition, emerging risks, such as cyber threats, develop over time, requiring review of insurance cover.

An RSA broker survey finds that while most SMEs identify new risks to their business, less than 20% of them have altered their insurance cover to match. It is likely that most SMEs find it easier to simply renew, rather than review, their cover annually.

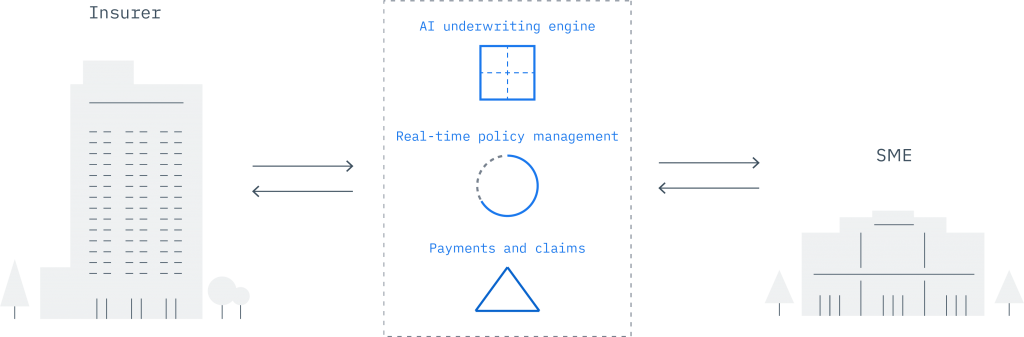

AI underwriting bridges the knowledge gap

SME customers increasingly want to buy insurance via seamless digital transactions. SME buyers also value expert advice; however, with 88% of brokers seeing underinsurance as a problem among SME clients, broker advice is currently not proving sufficient to tackle underinsurance head on.

At Cytora we work to build a different future, where data and AI is used to assess risks, and the assessment is available to both insurer and insured, meaning knowledge is equal and the scope of cover is understood equally by all.

This AI underwriting can help SME insurance buyers to understand the cover they need. By using external data from a range of sources, an AI underwriting engine can accurately predict characteristics about a business. It might suggest appropriate covers, and warn SME buyers when they risk underinsurance, or when the scope of cover is significantly different from similar businesses.

This technology also empowers insurance buyers to interact with their policy in real time, to update cover as their business grows, and to receive data-driven recommendations as their needs change over time.

About Cytora

Cytora is an artificial intelligence company powering a new way for commercial insurers to target, select and price risk. With the Cytora Risk Engine, insurers can improve underwriting profitability and reduce expenses while providing a frictionless buying experience to their customers. Cytora is backed by leading venture capital, global insurers and builders of some of the world’s most successful technology companies. For more information please visit www.cytora.com.