Selling Sprouts: The Future of Digital Life Insurance

Many of us working in life insurance believe we make good, socially useful products; I do, too.

Many of us also believe there’s a large mortality protection gap; I do, too.

Many believe that high sales friction is the biggest cause of this gap; I don’t.

To ensure more people get covered and in an effort to close the coverage gap, we need to ensure we tackle the right problem. Yet too often I hear the most frequent diagnoses of the problem focusing on friction at the point of sale, with comments such as:

“Underwriting is the problem: there are too many questions.”

“We’re losing sales because of friction in the underwriting process.”

“I need to make the product easier for customers to buy.”

Certainly, we should make our products easy to buy, customer journeys easy to understand, and underwriting no longer than it needs to be. But is friction during underwriting the biggest problem? Will reducing friction really help us materially close the protection gap?

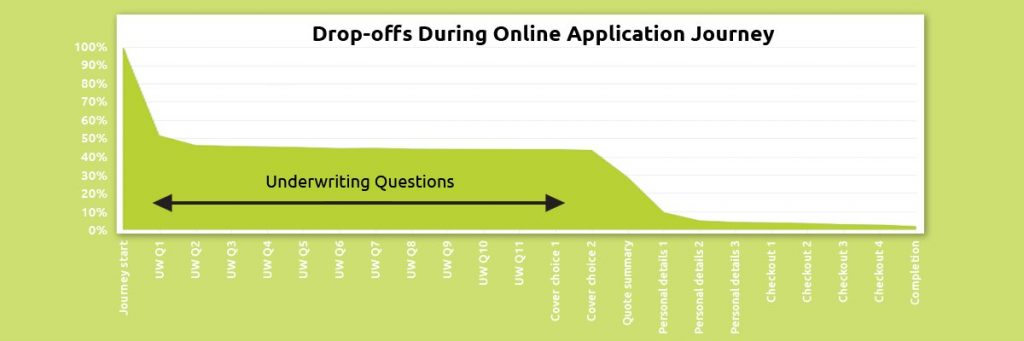

When the underwriting journey is sufficiently well-executed, the answer is a clear “No”. Here’s a chart showing drop-offs during an online application journey in the UK. Once we’d optimized the presentation of the underwriting section, virtually all the users who answered the first couple of questions also continued on to the last question. So, minor reductions in the number of underwriting questions will make no real impact on conversion rates.

Figures from an online sales journey for a UK Term Assurance product

The real problem is the high drop-off rate at the start of the journey and after underwriting is complete. To fix this problem, we need to think differently. We need to look at life insurance as if we’re selling Brussels sprouts. Yes, sprouts.

Know whether you are you selling sprouts or sweets

Imagine there are only two types of products to sell: sprouts and sweets. Sweets are an impulse purchase, so making them easy to buy should result in increased sales. So if you want to sell sweets successfully, the key is to reduce sales friction.

Selling sprouts requires persuasion

In contrast, as RGA’s Chief Behavioral Scientist Matt Battersby explains in “Role of Persuasion: How to Sell ‘Sprouts,” selling Brussels sprouts requires a different approach. Like life insurance, sprouts are good for you, but they’re also deeply unexciting: few shoppers will pick up sprouts on impulse. To sell these types of goods, you’ll need to use persuasion, create motivation, and provide an impetus to buy.

And yet, at every insurance industry conference and in hundreds of meetings with life insurers and reinsurers, the focus is on how to make underwriting slightly less frictional. Most of us are focusing on the wrong problem.

Misdiagnosing the problem is a costly mistake across the industry. Making something that people aren’t really inclined to buy slightly easier to purchase isn’t revolutionary; it won’t make a material difference to sales.

It’s the old adage about life insurance being “bought not sold.” Customers will seek out bought products because they already know they want them. In comparison, sold products, such as life insurance, are unfamiliar to buyers and aren’t often sold without prompting. Knowing whether your product is bought or sold is essential to growing sales.

So to get people to buy Brussels sprouts (and life insurance), you’ll need to do more than make the journey easy – you’ll need to add persuasion.

How to focus on the right problem

At many organizations, the innovation process is missing a key step: getting to the root cause of the actual problem. I’ve found a particular approach, called design thinking, is especially helpful in acquiring a very clear understanding of the exact problem. By putting the customer at the center of the process, it ensures you focus on their underlying problem. And by rapidly testing prototypes with real users, it avoids groupthink and reveals false assumptions before it’s too late.

Know when your problem is wicked

Misdiagnosing the problem is one mistake, but misdiagnosing the type of problem can be even worse. Closing the coverage gap, selling life insurance digitally (and selling sprouts for that matter) are examples of wicked problems: complex, messy, ambiguous and potentially impossible to solve in their entirety.

A few examples of the many wicked problems in insurance are:

- Creating engagement with life insurance customers

- Making health and wellness a priority

- Helping the aged population live happily

- Replicating the persuasion of face-to-face sales processes in digital channels

RGAX helps solve wicked problems. We’ve been traveling throughout the continents that make up our EMEA region – to Amsterdam, Dubai, Durban, London, Madrid, Nice and many more cities – to meet with carriers, distributors and technologists to explore the challenges and the opportunities of uncovering the real reasons why people aren’t buying life insurance.

Carriers across the globe are finding that these three themes resonate across cultures, geographies and languages:

- Understanding the nature of problems

- Being able to accurately diagnose and prioritize problems before taking action

- Employing a tested framework to find solutions to wicked problems in the insurance industry

Once you’ve identified why people aren’t buying life insurance, you are better equipped to develop strategies that persuade them.

Apply sprouts strategies to insurtech

A few people, like my son, love sprouts, so all you have to do is make them easily available. Most children, like my daughter, need more evolved strategies to get them to eat sprouts: they need to be persuaded.

The following digital insurance companies provide some examples of innovations that reduce sales friction and use persuasion to promote the sale of life insurance. They apply similar strategies used by parents to get their kids to eat sprouts:

1) Serve them with a nice meal. Yu life gamifies life insurance with a rich rewards experience, helping users to feel good (receiving rewards) while being good (consuming life insurance).

2) Focus on what they do for you, not what they are. The alcohol education charity, Drinkaware, found more success focusing on the effect alcohol has on appearance than on health. Similarly, insurtechs could focus on the impact a payout will have on the policyholder’s family, or engage in wellness conversations with customers using tools such as Quealth.

3) Know what motivates them. Selling sprouts to my son, who loves them, is very different to selling them to my daughter, who really doesn’t. Data-driven tools such as TrueRisk Life, a credit-derived mortality score from RGA and TransUnion, can help enrich an insurer’s understanding of potential customers and tailor processes accordingly.

Start selling life insurance via digitally persuasive channels now

As customers increasingly transact with businesses online, life insurers are struggling to create digital journeys that replicate the persuasive elements of traditional sales channels. The industry is experimenting and learning how to embrace the customer experience in a digital world. RGAX can help you. Start today with these four steps:

- DON’T focus on making sales easy (putting sprouts at the checkout)

- DO remember the importance of persuasion, even in digital journeys

- DON’T mis-diagnose the nature of your problems (some will be wicked)

- DO check out RGAX’s Life Design Sprints

Featured Resource: How to Accelerate Innovation in Life Insurance eBook

Get your guide on how to identify and move complex problems forward and champion transformation >>