Preventative insurance is here to stay

Let’s start with the obvious. Nobody wants to make an insurance claim.

Chances are – if you’re making one, you’re having a pretty bad day.

Insurance is a useful safety net for when things go badly wrong, but it has a lot of fairly game-breaking drawbacks.

To give you an example of one: a while back we commissioned a survey into UK homeowners’ most treasured possessions, and the lengths they went to in order to protect them. 30% of people in that survey said their most prized possession was something with negligible financial value – if not zero. Photo albums, childhood teddies and dolls, keepsakes and memories. Children’s artwork, baby clothes.

5% of people said it was the ashes of a loved one or a pet.

Insurance currently works by compensating us for the financial value of the things we’ve lost. But that’s not always a great remedial technology – none of those things above can be replaced by a pay-out. They are quite literally invaluable. Irreplaceable.

And it’s not just physical items.

What about the sense that your home is a safe place to live?

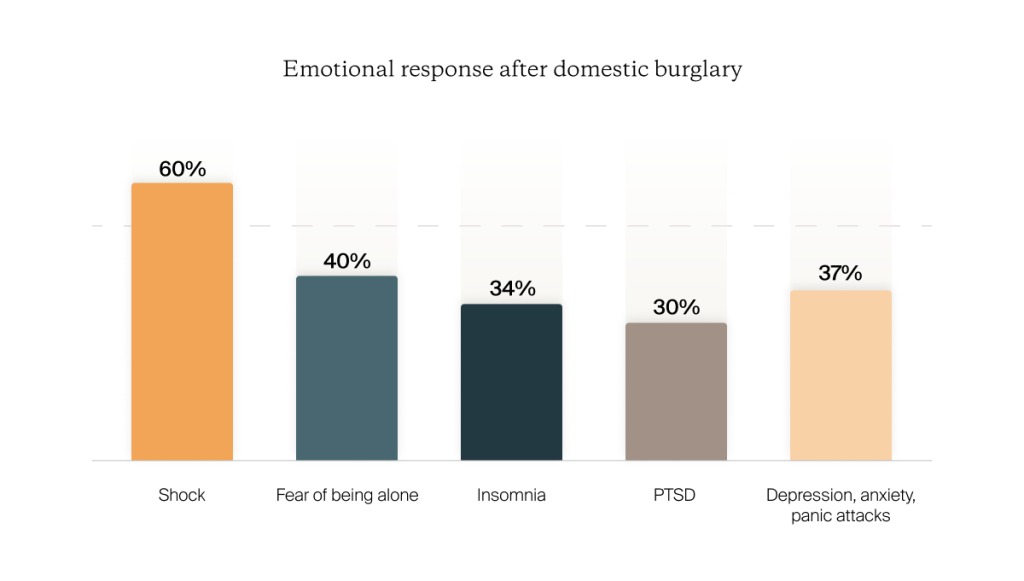

We’re driven by our “lizard brains”, by 200 million years of evolution, to seek shelters that are safe from threats like predators and fires. In the aftermath of something like a burglary, our lizard brains clamour incessantly that our “cave” is no longer safe; that we are still in danger, that we must not sleep or rest. 60% of people report never feeling safe in their own homes again; 34% develop insomnia, 30% PTSD. About 1 in 7 has to move house just to shut the lizard brain up.

These things cannot be paid off. They can only be protected.

With all this in mind, we’ve been working on a new kind of insurance for a couple of years now.

You could call it “proactive insurance”.

Or preventative insurance.

Or protective insurance.

Either way, our manifesto is the same:

People buy insurance to protect the things they love. Insurance companies like to portray themselves as “umbrellas” – a protective shield to keep the rain at bay.

But in reality, pay-outs do nothing to protect you. They’re more like a towel than an umbrella.

They’re not even a very effective remedial technology, because so many of the things we value most can never be replaced.

At Locket, we’re building insurance that helps you prevent bad things from happening in the first place.

You’ll always have the safety net of pay-outs as a second line of defence, but the goal is to ensure you never even need them.

How does it work?

Let’s zero in on home insurance, because that’s what we currently specialise in at Locket.

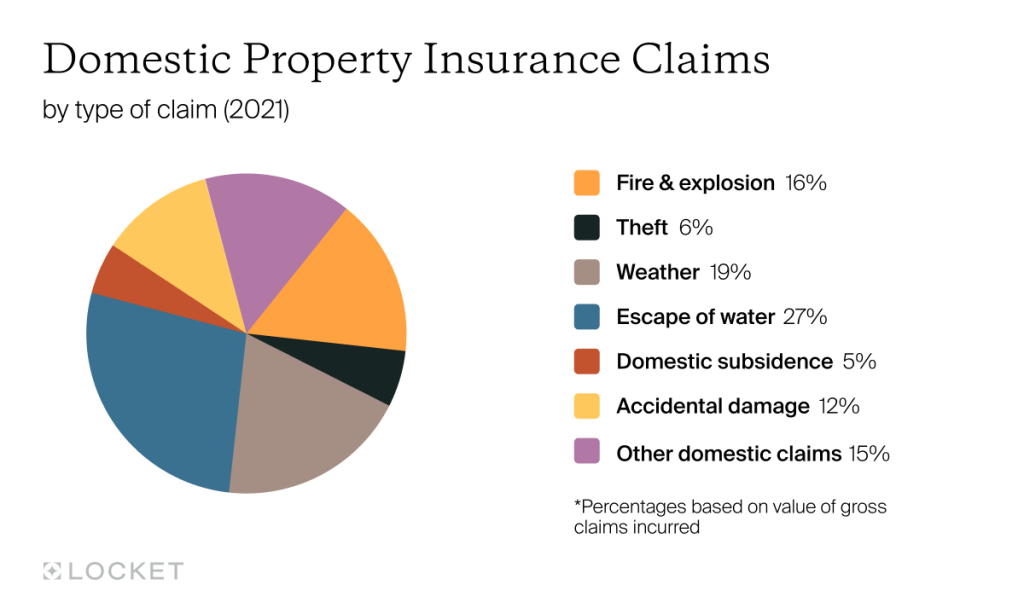

In an average year, insurers pay out around £16m a day for damage to UK property – about £5.8 billion a year, with a roughly even split between domestic and commercial property claims.

If you ask a hundred people on the street to guess the most likely things to damage their home or belongings, factors like fires and burglary consistently come out on top.

In reality, the causes of that damage break down something like this:

Depending on the technology we apply, somewhere in the region of two-thirds of claims are theoretically preventable.

That represents potential efficiencies of nearly £10 million a day. Every day.

Let’s talk about escape of water first.

It may surprise you to learn that “escape of water” – water leaks – account for about as much damage as all fires, explosions and theft combined; nearly a third of the pie chart in domestic environments. They also waste something in the order of three billion litres of water every single day, in the UK alone. And they’re one of the most preventable, as we’re about to discuss.

Locket has been quietly equipping a group of customer volunteers – we call them “Insiders” – with something called “Sonic” for a few months now. Sonic is a whole-home leak detection system. Your plumber cuts the incoming water main and installs Sonic right after the main shut-off valve for your home. From there it has an eagle-eye view of all the water that flows into your home, and it samples it up to 86,000 times a day, around the clock, with an array of four different sensors (ultrasonic flow meter, pressure and two different temperature sensors).

This sophisticated array of instruments allows Sonic to detect if there’s a leak anywhere in the fresh water system of your home. And if there is, it notifies you via a companion app – and can even shut off the water to prevent damage.

In the four months we’ve been equipping customers with Sonic, 4% have already had an escape of water claim prevented. That suggests in a full year, something like 12% might see a “protection event”.

Escape of water claims are £1.2bn of all claims (commercial and domestic combined); 12% of that is ~£144 million.

But that’s barely even scraping the surface.

In 2019, another leak detection solution called Flo by Moen ran a pilot in 2,300 US homes, measured against a control group of 1.3 million homes not equipped with Flo. Over a two-year time period, they reduced escape of water claims by 96% in their sample using the Flo technology.

Ninety-six percent.

Even the four percent who filed claims did so at a 72% value reduction versus the industry mean.

Running the UK figures again, that could mean reducing the £1.2bn total claims by around £1.15bn.

Starting to see how exciting this is?

So what about fires and thefts?

While water leaks are the largest issue from the claims point of view, smart tech can prevent or minimise other threats – in particular thefts and to some extent fires, too.

Locket has also been working with a range of leading manufacturers like Ring and Yale to equip our Insiders with security and safety technology. Between the raft of technologies, up to 11% have seen a “protection event” in the past four months – a probable prevented claim. We say “up to 11%”, because we’re dealing in hypotheticals here – it’s difficult to say how many of these close shaves would have resulted in claims. But here are a couple of examples:

We can’t predict the future (not yet, anyway). But it’s reasonably clear these could have resulted in loss or damage.

Up to 11% in four months. So – up to 33% claims reduction in a year? It’s amazingly close to the result of another study we ran in 2020, this time a retrospective of 3,000 randomised UK homes, which found that homeowners who had protective smart home devices were 35% less likely to have suffered a major insurance claim (>=£5,000) in the five years prior.

We don’t want to overstate our case here, but at the same time, we’re just getting started.

By the end of 2022 we’ll have released at least two new protective technologies:

- A “mockupancy” mode, which harnesses smart devices like lights and speakers to pretend you’re home even when you’re not. 86% of burglars say they avoid occupied homes altogether, and that point was brought home during the pandemic when burglaries fell 28% during lockdowns.

- A crime map that draws on police data to show you detailed stats on the crime in your area, or any area, so you can learn about the specific risks and get tailored advice on how to stay safe. We’re working on making it context-aware, too – so you might get a notification to say “bike theft rose 65% in your neighbourhood this summer. Here’s a guide written by an ex-bike thief on how not to become a victim”. Locket members will also get offers on complementary technologies like bike locks, GPS trackers or outdoor cameras.

And when they set those technologies up, their Locket insurance might get cheaper, too.

Because that’s arguably the most powerful piece of the puzzle: behavioural economics and habit-forming education.

These aren’t completely new in insurance – the health sector has used them effectively for a number of years now. “Buying health insurance? Here’s a free FitBit activity tracker, or a discount on gym membership.” The more sophisticated programmes tie in activity tracker data or gym attendance to the policy and offer increasing rewards or discounts for regular usage. In one study, a large corporate decided to give employees FitBits as well as company health insurance. Employees who took the activity tracker were 24.5% less likely to claim on their health insurance over a two-year period – equivalent to a saving of $1300 per person, $2.3 million overall.

The eagle-eyed readers will have spotted the elephant in the room here: did FitBits make those employees less risky, or was it that more-health-conscious employees were more likely to accept the offer of a FitBit? The study did take pains to compensate for that, factoring in data from the two years prior as well. But from an underwriters’ point of view, recruiting less risky customers by default is a serious benefit – not an experimental flaw.

So what do you think?

We believe it’s the future.

Customers getting more of what they really want from insurance – safety, security, peace of mind; protecting the things that matter, and crucially the things that can’t be replaced. And even better – paying less for their insurance, because insurers are saving millions, billions even, on prevented claims.

Preventative insurance is here, and it’s here to stay.

Media enquiries

Rob Balderstone, CMO