Partnering for Innovation in Insurance: Tackling the Industry’s Biggest Challenges

Innovation is a top priority for many life and health insurers. In this recent article, RGAX explored how partnering can help carriers overcome many of the obstacles to innovation in our industry. I’d like to continue the conversation by focusing on examples from the work we are doing to build connections between carriers and insurtech startups.

Uncovering Opportunities for Innovation in Insurance

A potential innovation partnership can be triggered in a variety of ways. Because of the work we do in the industry, RGA and RGAX are in a unique position to spot opportunities and join in industry conversations happening at all levels and parts of the value chain. We are always looking to draw out problem statements from our clients and industry peers. Our parent company, RGA, has relationships with numerous life and health insurance providers of all sizes, across the globe. In partnership with RGA, RGAX works with insurtech startups addressing the most pressing challenges and opportunities in our industry. We’re on the frontlines of innovation in insurance and health.

There have also been instances when carriers come to us with an opportunity. For example, they may want to tap into our network to help them address a challenge more quickly or effectively than they could have by building in-house capabilities or processes. Many insurtech entrepreneurs have worked in the health and insurance industries. They start their businesses based on a challenge they’ve personally experienced. By coming to us, we can help them connect with carriers that can provide testing, validation, and a ready market to get their ideas off the ground.

Here are some prime examples of insurtechs we’ve been working with and the challenges they’re helping to solve:

OWL is an example of when the carriers we work with came to us with a problem: identifying fraud in disability claims. RGAX recognized Owl as the right insurtech partner to help solve this challenge. Owl uses publicly available data to take an unbiased approach to identifying possible fraudulent claims so that a carrier can conduct a deeper investigation. For each fraudulent claim uncovered, the carrier can free up anywhere from $60,000 to $250,000 of reserves that they had to hold for each claim. As an expert in privacy rules in the jurisdictions in which they operate, OWL may also help carriers avoid running afoul of local rules and regulations.

ManagingLife is another example of an insurtech we’re working with to help address a disability claims business challenge. Roughly 20% of all disability claims concern chronic pain or muscular-skeletal (MSK) issues. By providing tools and information to help individuals manage their chronic pain and do a better job of sharing feedback in near real time with care providers, ManagingLife can help them get back to work more quickly and improve the claims experience. RGAX is working with ManagingLife to develop relationships with carriers to offer this service to claimants.

Read how RBC Insurance used ManagingLife to lower long- and short-term disability claim duration.

HealthPals is an example of a partnership initiated from the insurtech side, even though the challenge is one readily recognized by carriers: the need to drive down the cost of care. RGAX is working with HealthPals to help carriers apply AI to care management. At scale, this allows them to offer better care management strategies through healthcare providers to improve outcomes and lower costs.

Moody Month is a startup emerging from the femtech market. Their daily health and wellness tracker app connects women with solutions to support their most common moods. RGAX has partnered with them to design an insurance proposition that empowers women and transforms their access to insurance and financial information.

Pendella is a company that helps carriers innovate their business model by providing them access to API-driven life and disability product solutions for agents or direct-to-consumer (D2C), which are all geared to improving the user experience. We introduce Pendella to the carriers and distributors we work with when it makes sense as a solution to the challenge or opportunity at hand.

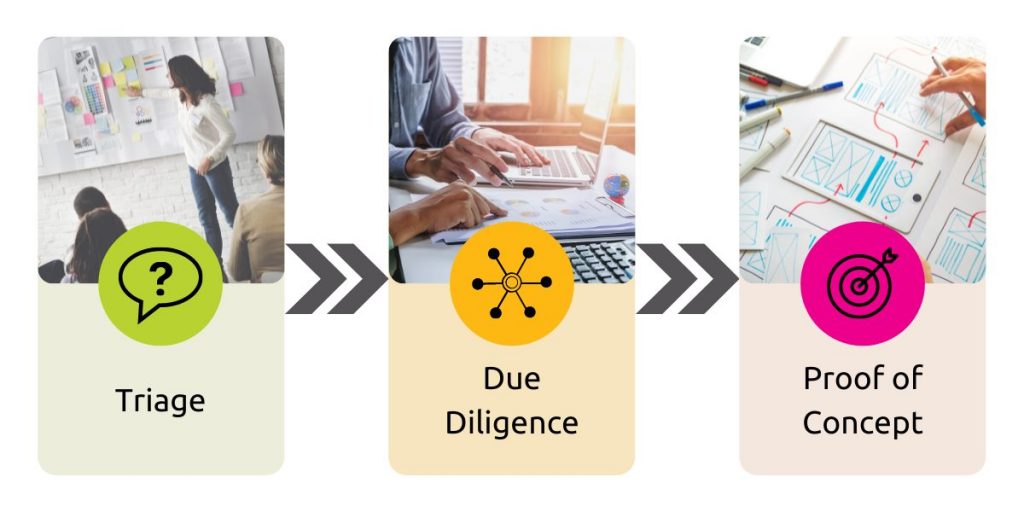

The RGAX Insurtech Partnership Lifecycle

While each partnership we create is unique, the lifecycle of partnering with RGAX follows a defined pattern.

- Stage One: Triage – At this stage, we’re talking to a prospective insurtech partner that may fill a need we’ve identified or that has presented a compelling business case. Our team’s job is to determine how “real” the opportunity is and what our next steps should be. If we’re working with an insurtech startup, we’re evaluating its progress, among other things. It’s not that we don’t want to hear from early-stage innovators, but we’re far more likely to enter into a partnership with a startup that already has a proven solution.

- Stage Two: Due Diligence – If the partnership opportunity looks compelling to our innovation team, our next step is to do a deeper dive with our subject matter experts. For example, if the solution is focused on accelerated underwriting, we’ll bring in our underwriting experts to take a look. We’ll also assess whether the insurtech has a customer using the solution and whether that customer is happy and willing to provide a testimonial.

At this stage, we’ll also evaluate the insurtech’s ability to navigate the carrier’s procurement department. This is one of those hurdles that can derail even the most enthusiastic entrepreneur. If they’ve never worked for a large enterprise, they may not understand the power procurement wields and how difficult it can be to get approved.

- Stage Three: Proof of Concept – By stage three, we’re comfortable with the business case for the opportunity, or the insurtech wouldn’t have made it this far. Still, fine-tuning must be done, which includes further detailing costs, modeling the ROI, defining a mix of qualitative and quantitative success measures, and demonstrating scalability.

During stage three, we’ll also outline a marketing agreement. There are no boilerplates here. Each agreement is based on the opportunity and where the partner is in its lifecycle. Some of these agreements may involve an investment of capital, while others may focus on providing guidance during the evolution of the companies involved and strategies for expanding market reach.

Take the Next Step with RGAX

Ready to innovate? Whether you’re a carrier looking to solve a challenge or an insurtech with an innovative solution, we want to hear from you. Together, we can make transformation happen. Let’s Connect.

Featured Resource: How to Accelerate Innovation in Life Insurance eBook

Get your guide on how to identify and move complex problems forward and champion transformation >>