Coventry hits Abacus with three counterclaims

Coventry First and chairman Alan Buerger filed their answer and counterclaims against Abacus Global Management on July 9, escalating a legal battle over life expectancy estimates and the valuation of life settlement policies.

The 97-page filing, submitted in the U.S. District Court for the Middle District of Florida, denies Abacus’s remaining claims and argues that the statements at issue were true. Coventry also brings three counterclaims: one under the Florida Anti-SLAPP Act and two under the Florida Viatical Settlements Act.

Coventry is seeking compensatory and punitive damages, lost profits, attorneys’ fees and costs.

At the center of the dispute is Lapetus Solutions, the now-defunct life expectancy provider previously used by Abacus. Coventry alleges Abacus knowingly used life expectancy estimates from Lapetus that were systematically too short to increase the reported value of its policies and generate gains through sales to affiliated funds.

“Abacus’s lawsuit is thus not a legitimate effort to remedy legitimate legal claims. It is the culmination of Abacus’s knowing scheme to use Lapetus’s misleading and deceptively short life expectancies for its own financial gain.”

Coventry cites its May 2024 study, which found that Lapetus produced shorter estimates in approximately 85% of matched cases. It also points to a July 2024 analysis by professors Daniel Bauer and Nan Zhu, which found shorter estimates in 83% of cases, with Lapetus averaging approximately 29 months shorter.

A February 2025 update cited in the filing placed Lapetus’s actual-to-expected ratio at 31%, compared with more than 90% for other providers.

“On February 5, 2025, Professors Bauer and Zhu found that Lapetus’s Actual/Expected Ratio for the studied population was a catastrophically low 31%—confirming that Lapetus LEs are well shorter than the actual lifespans of the individuals they are providing LEs for. In fact, other, more wellregarded LE providers have Actual/Expected ratios that exceed 90%.”

Coventry also quotes Lapetus’s former CEO explaining his decision to resign: “I don’t trust [Abacus],” and “can’t in good faith continue to work with ABL.”

Another counterclaim focuses on Abacus CEO Jay Jackson’s relationship with Lapetus. Coventry alleges Jackson served as a voting member of Lapetus’s board from November 2021 through November 2024 while also serving as an officer and director of Abacus and its affiliates.

Coventry argues that the arrangement violated Florida’s prohibition on viatical settlement providers serving as directors of life expectancy providers. It also alleges that Jackson used his board position to share Coventry’s confidential trading information, including its volume and trading patterns, with Abacus employees. Coventry says it uncovered this information during discovery.

“Jay Jackson held a position on Lapetus’s board, which “may” have violated Florida’s “Life Expectancy reform law.” Id. Abacus admittedly invested in Lapetus. And Abacus did in fact bizarrely claim that Lapetus “provides the most conservative” life expectancy predictions—even though all evidence is to the contrary.”

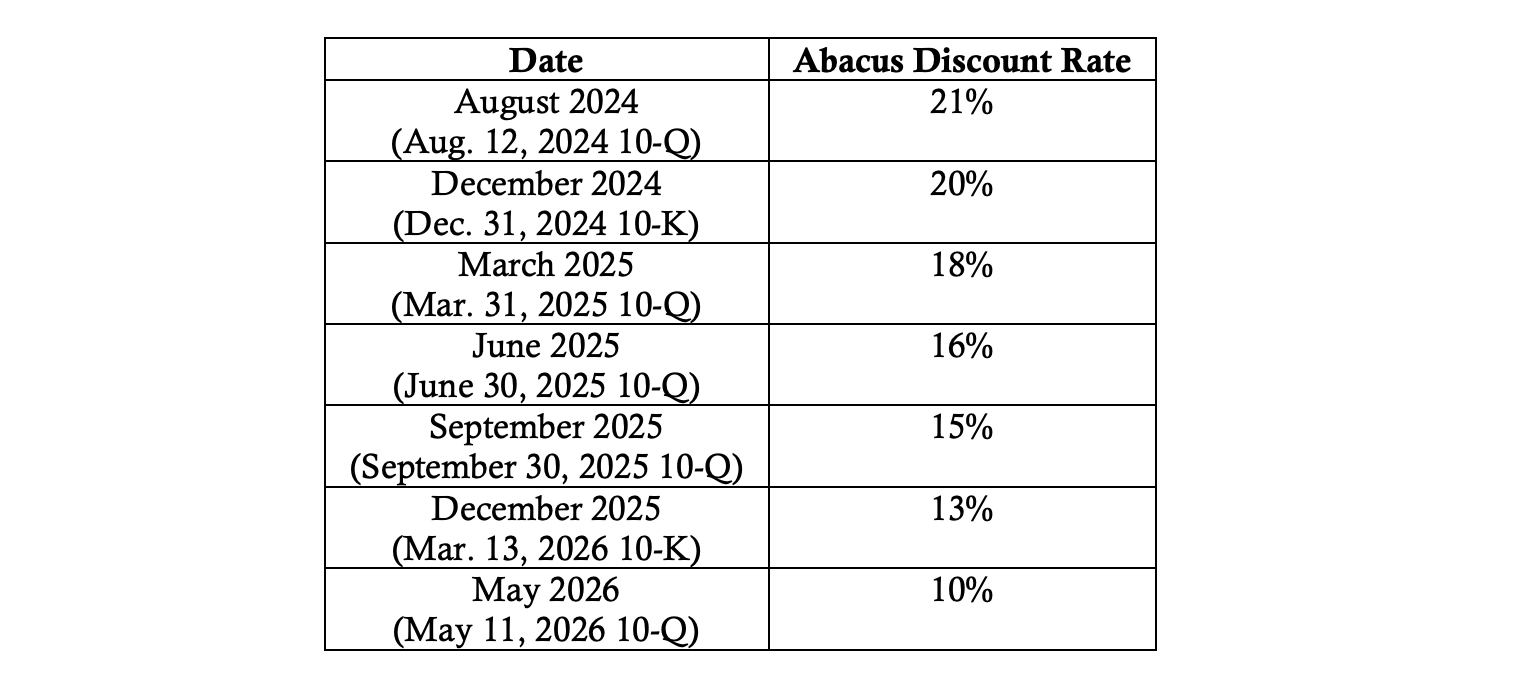

The filing also challenges changes to the discount rates Abacus used to value its policies. According to a table included in the filing, Abacus lowered its disclosed discount rate from 21% in August 2024 to 10% in May 2026, with reductions occurring each quarter.

Coventry claims Abacus initially used the higher rate to offset the effect of Lapetus’s shorter life expectancy estimates. Once questions about Lapetus became public, Coventry alleges Abacus began lowering the discount rate, with each reduction increasing the present value of its portfolio. The filing notes that Abacus’s external auditors identified the determination of discount rates as a “critical audit matter.” Coventry says the auditors were later dismissed.

Coventry also challenges Abacus’s sales to affiliated investment funds. It alleges that more than 78% of the policies Abacus sold in 2025 went to related parties, including four funds managed by the company. In the most recently reported quarter, that figure increased to 92%, according to the filing.

Those funds have raised more than $500 million, primarily from credit unions, after being marketed as offering stable, bond-like returns, Coventry claims.

“Abacus used its own clients’ capital to monetize the policies at prices no arm’s-length buyer would agree to.”

Coventry cites an Abacus filing showing average realized gains of 26.4% on related-party sales, compared with 10% on sales to outside buyers.

The filing also questions an actuarial review conducted by Lewis & Ellis that Abacus promoted in June 2025. Coventry alleges Abacus influenced the results by supplying internally generated life expectancy estimates for more than one-third of the policies reviewed and selecting older, shorter estimates for other policies.

In one example, Coventry says Abacus provided Lewis & Ellis with a single 86-month estimate from December 2018 even though it possessed at least 10 newer and longer estimates for the same insured.

By relying on the older estimate, Coventry alleges Abacus “created nearly [redacted] in value out of thin air on just this policy alone.”

Coventry denies any involvement in the June 2025 report published by short seller Morpheus Research, which Abacus linked to a 21% decline in its stock price. According to Coventry, a Morpheus representative testified under oath that neither Coventry nor Buerger participated in preparing the report.

Coventry claims Abacus instead sued the industry participants who had publicly raised concerns about its practices. It describes the lawsuit as “a warning shot—a transparent attempt to silence public debate about Abacus’s practices as a public company.”

On June 26, the court allowed three of Abacus’s claims to move forward: defamation, defamation by implication and a claim under Florida’s Deceptive and Unfair Trade Practices Act. The court dismissed claims for defamation per se and tortious interference.

Abacus held its Investor Day at the New York Stock Exchange on July 16. The company has not publicly responded to Coventry’s counterclaims.