Cheap, Powerful, So-called Insurance Brands

You’ll soon see that a certain someone said that the insurance industry is where the travel industry was 10 years ago. While I don’t remember what the travel industry looked like ten years ago, I doubt that the Four Seasons would bid on the Google search term ‘cheap hotels in NYC’. Why? Because Four Seasons and cheap don’t go together; not if you ask their CEO, their advertising agency, and the average Joe that’s looking for a hotel.

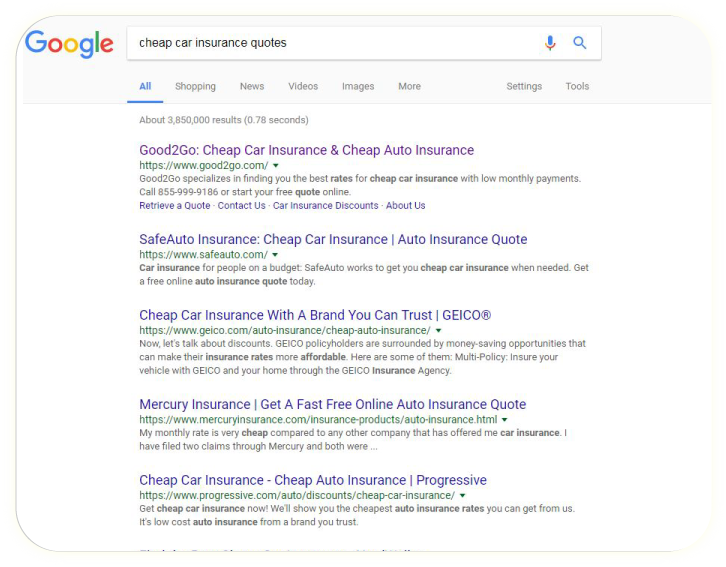

And yet when you search Google for ‘cheap car insurance quotes’, you’ll find leading insurers like GEICO, Progressive and Nationwide competing for the first place using cheap terms, quality terms, or any other terms for that matter. Why? Because leading insurers don’t really care about a defined message, or about their brand, they care about their business .

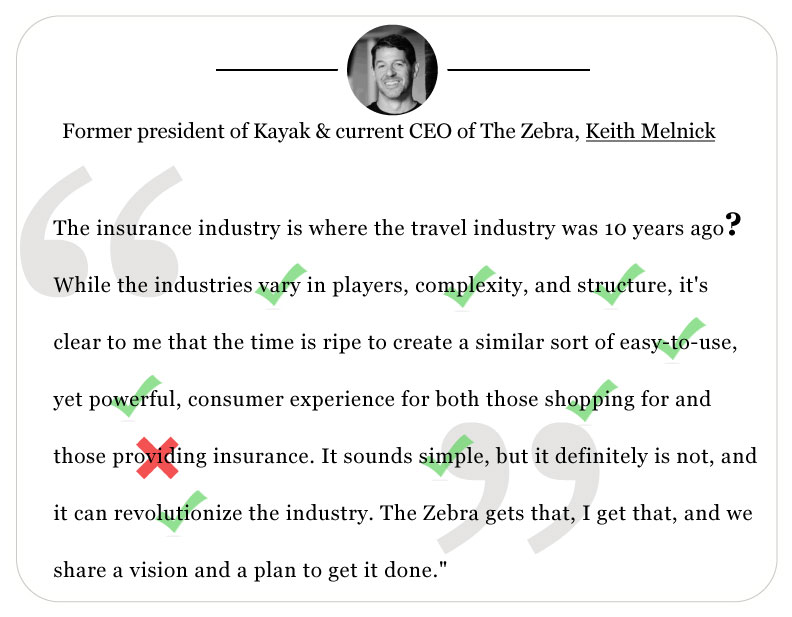

Keith Melnick is right (think: The Zebra’s new CEO). He’s right about the time being ripe for creating a platform similar to Kayak, not just for auto insurance, but for any kind of insurance. He’s also right about the fact that it won’t be simple and it will revolutionize the industry. But, Keith is also wrong. He’s wrong about the part where he mentions the experience for “both those shopping for and those providing insurance.” Don’t get me wrong, giving consumers the ability to compare accurate auto insurance quotes in one platform and in real-time, just like with Kayak for travel, is a dream come true for any consumer, but it’s also the worst nightmare of any insurer .

Sort by price; good for consumers, bad for insurers.

The “sort by price” filter is probably the most popular filter on comparison platforms. But what’s good for the travel industry is bad for the insurance industry. When consumers look for a hotel for their vacation, they are wise enough to understand the difference in prices between one hotel and the other. They understand that hotel prices are based on different factors such as: location, service, food, etc. and usually, you get what you pay for. Imagine what would happen if there was a comparison site for auto insurance – consumers will sort by price from low to high and probably go for the cheapest option, even if that option is called Average Coverage Insurance Services, LLC. Most consumers can’t understand or justify the difference in rates between policies; if the coverage is the same then the rate should be the same. This isn’t a 4 star insurance policy vs. a 5 star insurance policy. And it’s not just for first time shoppers, it’s also for renewals, just look at what’s happening in the UK:

Consumers don’t trust insurers. Insurers don’t trust consumers.

Let’s agree, or agree to disagree. Right now, leading insurers are firing on all cylinders to get business. This includes TV, Google, social media, Lead-Gen companies, and any other medium that can deliver their message. Unlike the travel industry, insurance isn’t seasonal. For companies like GEICO, every day is an opportunity to attract new clients from competitors. But, that’s not the only reason; it’s also because there is no customer loyalty in insurance, after all, how can loyalty be created when its main factor is something that constantly changes – price. Lack of customer loyalty is something insurers are aware of. And because of that, they won’t give up control to a single platform, which will display them in a small box, next to their competitors, with advanced filtering options.

Rings of Power.

Hotels are fighting Expedia and Priceline, and while it may be too late, they still have a fighting chance thanks to their brand. If you’ve watched Lord of The Rings, you know the story about the rings of power created by Sauron. You probably also know that Sauron created one secret ring that will rule them all. I’m not saying that Expedia and Priceline are the evil Sauron in this story, but do you remember how they started? They were small & friendly. They tried very hard to get hotels on board. Once they did, they grew to be so powerful that they now control their industry. Insurance companies are pessimists by nature; they think about the worst case scenario – it’s what they do. Kayak, Expedia, or Priceline for the insurance industry is their worst case scenario, and they will do everything they can to prevent it from happening.

The fear factor.

The fear factor is often used in insurance. This time however, it’s not for driving sales, it’s for driving an entire industry in a certain direction. While leading insurance companies understand that a platform that gives consumers control is a point of no return, it’s really not up to them. At the end of the day, consumer-friendly platforms will always win, because that’s what consumers want – just look at the control Expedia, Seamless, Amazon and Uber have on their industry. And this is another factor insurance companies are aware of. The question is will fear drive insurance companies to give up control to one single platform, or will they maintain their position to control their destiny.

Get Coverager to your inbox

A really good email covering top news.