The Importance of High-Precision Geolocation in Wildfire Risk Estimation

Acres burned by wildfire in the US have climbed year after year since the early 1980s, increasing in both frequency and intensity. In California, the Butte County Camp Fire in 2018 was the costliest wildfire in modern history, burning 153,336 acres, destroying 18,804 buildings and claiming 85 lives, stoking heightened interest amongst insurers and reinsurers to manage this risk effectively.

For insurers and reinsurers, one of the best methods to manage wildfire risk is to proactively account for it during the pricing and underwriting process. The necessary prerequisite is to ensure that all relevant risk factors are considered at the property level. This includes nearby fuel sources and the structure’s distance to those sources, defensible space, wildfire history, types of vegetation, slope, aspect, average rainfall, katabatic wind areas, the time required for first responders to arrive on scene, and many other variables. However, without first knowing the insured building’s actual geolocation, how can all these wildfire risk factors be accurately determined at the property level?

Ecopia.AI, in partnership with Black Swan Analytics LLC, explored the impact of accurate building geolocation on wildfire risk assessment. As the creator of a proprietary, highly sophisticated and predictive wildfire model that includes all of the above factors, Black Swan was the best choice to explore the pitfalls of using the industry-standard parcel-based geocoding.

Since California faces severe wildfire risk, Ecopia picked two counties within California to analyze – Trinity and Modoc – each representing different characteristics, to assess the impact of geolocation on wildfire risk. To conduct the research, Ecopia and Black Swan calculated wildfire risk scores for over 30,000 properties, comprising every property in both those counties, using two separate approaches. First, a wildfire risk score was calculated using each property’s parcel centroid as the geolocation (the centre of the parcel), then the wildfire risk score was calculated using the building’s actual geolocation via Ecopia’s building-based geocoder (based on Ecopia’s proprietary database of all 170M+ building footprints in the US generated from high-resolution satellite imagery).

The results showed a clear conclusion: by using parcel-based geolocation, 25% of the properties were mispriced across the two counties (defined as a significant difference in risk levels). In the case of Trinity County, 29% of properties were mispriced (12% underpriced, 17% overpriced). Figures 1 through 3 highlight the results of this study.

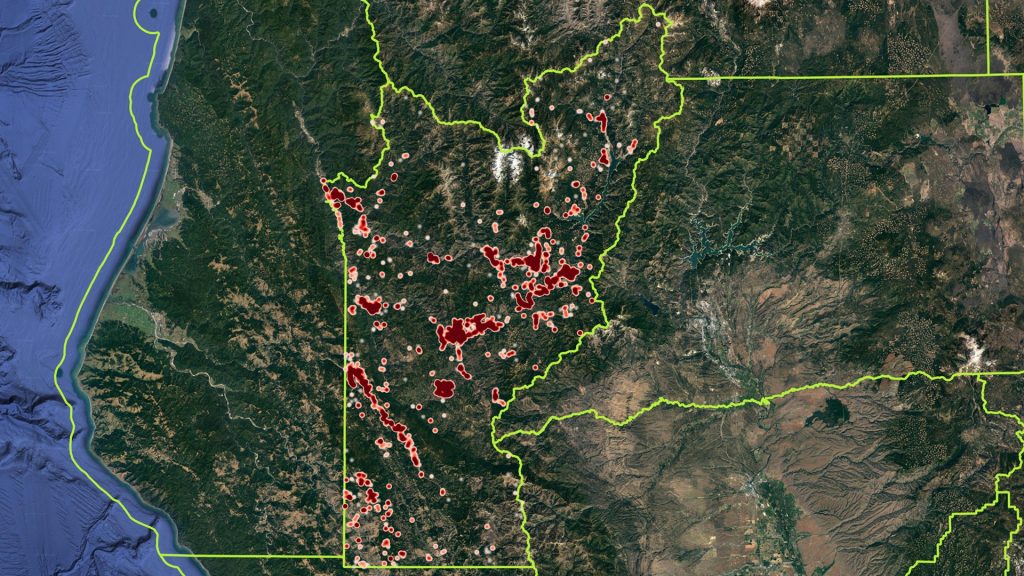

Figure 1: Heatmap highlighting mis-pricing across Trinity County.

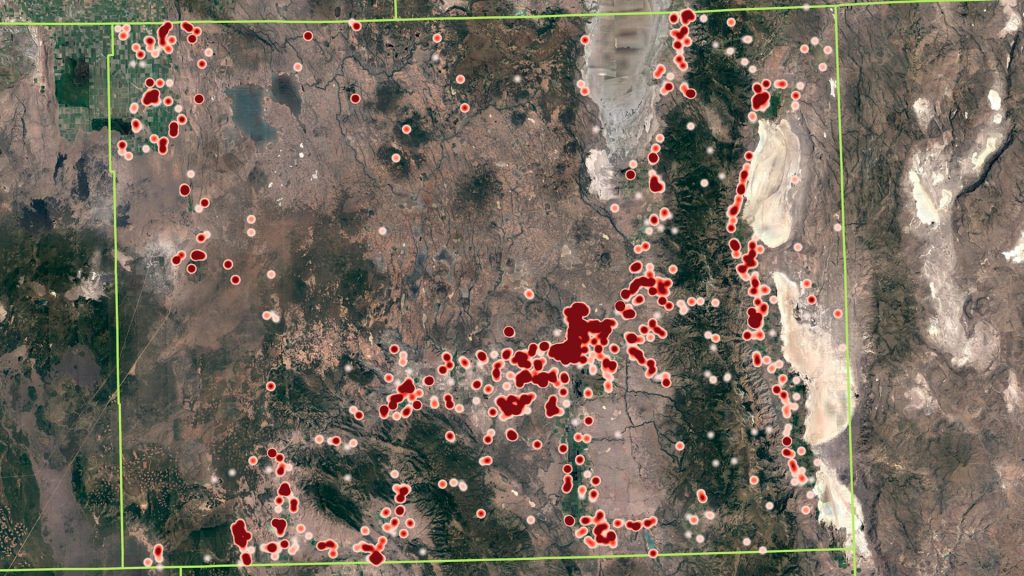

Figure 2: Heatmap highlighting mis-pricing across Modoc County.

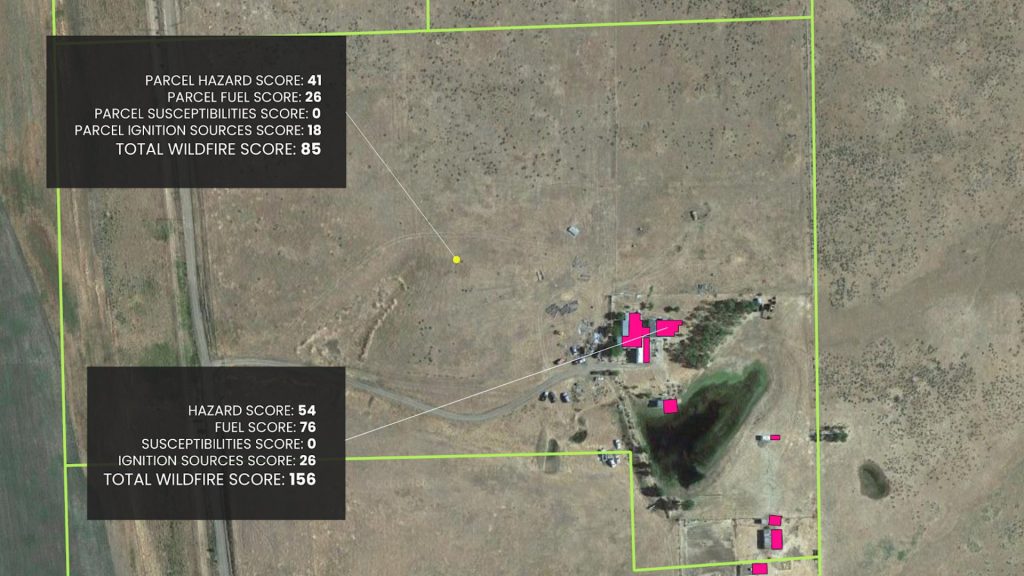

Figure 3: Example of mis-pricing based on inaccurate (parcel-based) geo-location.

Viewing the above example, you can see that based on the parcel-centre geolocation (middle of a barren field), the risk score of 85 would fall in the Low-Moderate Risk category. However, inputting the actual geolocation of the building (near other buildings and brush) would result in a risk score of 156 – well within the High-Risk category. In the US property insurance industry, mispricing to this degree would result in a significant difference in policy premiums and/or underwriting acceptability. Not only are insurance portfolios exposed to substantial hidden risk through underpricing scenarios, but policyholders who are overpriced may search for pricing closer in-line with what they perceive as fair, given the actual location of the building on the parcel. If this continues, the carrier will be left with only those policies that are underpriced. These inaccuracies will consequently drive premiums upward for all customers, through base rate increases – making the insurer increasingly less competitive over time.

In summary, when assessing a property’s wildfire risk, a precise understanding of geolocation is paramount. An inadequate grasp of a building-based geolocation introduces significant unsubstantiated risk. For insurers looking to underwrite with confidence, building-based geocoding provides an accurate understanding of risk – allowing insurers to more accurately select and price the risks they choose to insure.

To learn more, please contact [email protected] or [email protected].