White Mountains would rather buy electricians than insurers

White Mountains used its annual investor presentation on June 5 to make a case for patience. After cashing out of Bamboo Insurance, the company is finding more opportunities in electrical contracting than in traditional underwriting.

The numbers are hard to ignore. Book value per share (BVPS) increased 25% in 2025 to $2,188, one of the company’s best years on record, helped by the December sale of Bamboo Insurance to CVC Capital Partners at a $1.75 billion valuation. White Mountains invested roughly $300 million in the homeowners MGA, received about $1 billion in cash at closing, and retained a 15% fully diluted stake valued at approximately $250 million. The investment generated a 4.1x multiple on invested capital (MOIC) and a 113% internal rate of return (IRR). Management called it a “deal you don’t refuse.”

The bigger story is where that capital is being redeployed. White Mountains Partners, the wholly owned acquisition vehicle launched in late 2023 to acquire founder- and family-owned businesses, has invested roughly $200 million across three electrical services businesses: Enterprise Solutions, an electrical contractor acquired in April 2025; BaseSix, a low-voltage electrical systems company acquired in April 2026; and Hawkeye, a bolt-on acquisition completed in May 2026. Together, the businesses represent about $34 million of adjusted EBITDA acquired at a weighted average multiple of roughly 9x. The unit will become a standalone reporting segment this year, with up to $500 million earmarked for additional acquisitions.

Where White Mountains has invested in insurance, it has largely favored fee-generating businesses over underwriting risk. The company invested $225 million for a controlling economic stake in Distinguished Programs, an MGA that earns commissions rather than retaining insurance risk, with an agreement to acquire an additional 31% in 2028. It also committed $125 million to Bishop Street through a structured investment alongside RedBird Capital Partners and invested $150 million in BroadStreet Partners, the insurance brokerage. The common thread is ownership of distribution and fee income rather than catastrophe exposure.

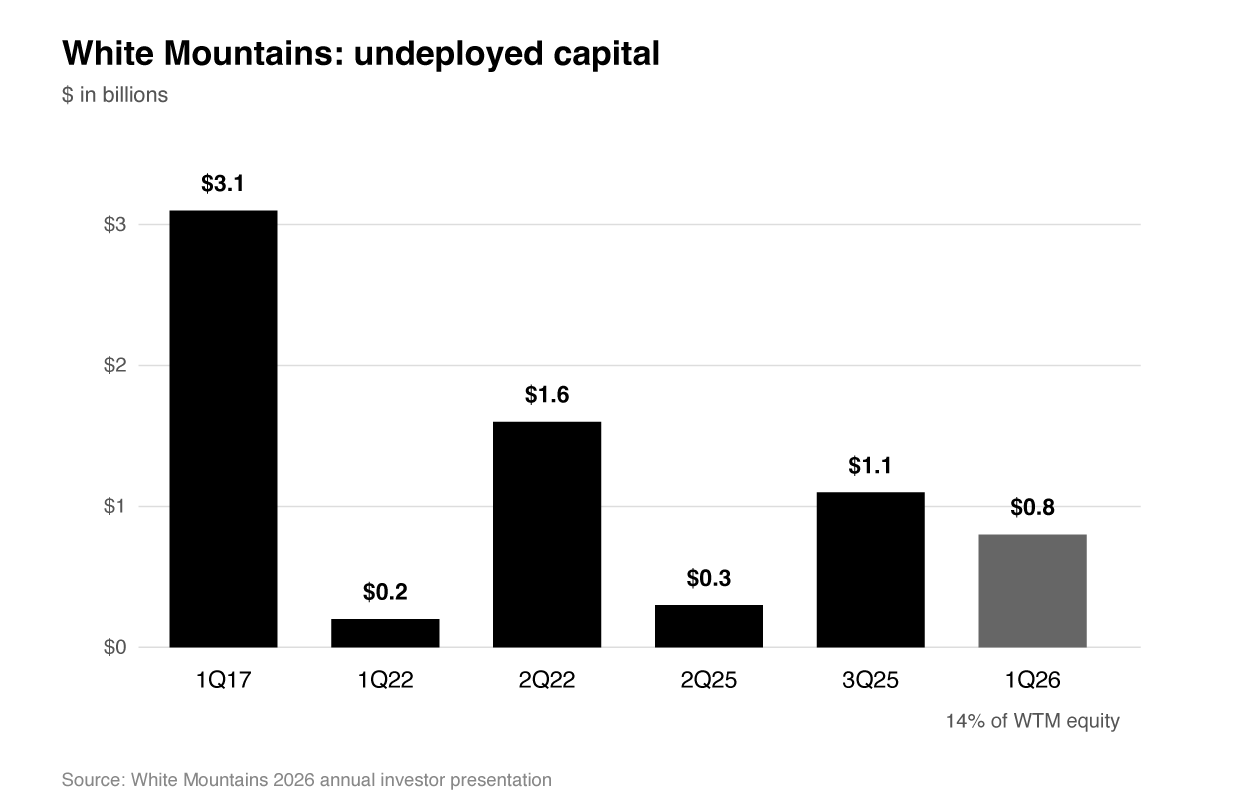

White Mountains enters the softening insurance market with $7 billion of total capital, no parent-company debt, and approximately $800 million of undeployed capital—about 14% of shareholders’ equity. By comparison, the company held $3.1 billion of undeployed capital in early 2017. Management described the current (re)insurance deployment environment as “challenging” and emphasized patience. The balance sheet suggests it’s willing to wait for better opportunities.

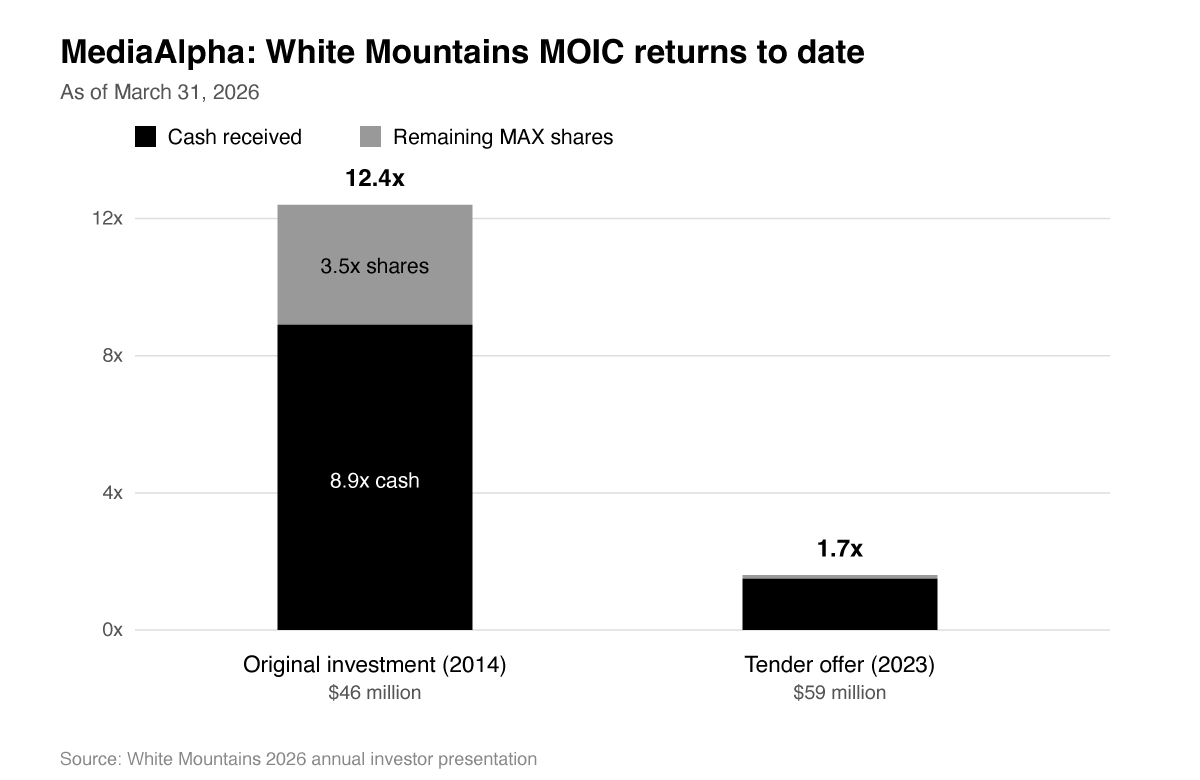

One investment that stands apart is MediaAlpha . White Mountains owns a 28% stake in the online insurance customer acquisition platform, or 17.9 million shares, valued at $166 million as of the first quarter of 2026, and no longer holds a board seat. Management described 2025 as a “mixed year.” MediaAlpha delivered record operating results, with revenue rising 29% to $1.1 billion and adjusted EBITDA increasing 18% to $114 million. The company settled its FTC matter related to its under-65 health insurance business, authorized a $50 million share repurchase program that was later increased to $100 million, and saw its shares rise from $11.29 to $12.95 during the year. Despite reporting another strong quarter in 2026 and continued momentum in its P&C business as carriers increased advertising spending, the stock fell to $8.90 by May 31. White Mountains attributed the decline to sector-wide multiple compression rather than company-specific issues. The investment has nonetheless been a success: White Mountains’ original $46 million investment in 2014 has generated a 12.4x multiple, with 8.9x already returned in cash.

The presentation also marked the final investor meeting under CEO Manning Rountree, who retired at the end of 2025 after leading the company for 21 years. During his tenure, adjusted book value per share compounded at 13% annually, while White Mountains returned $2.3 billion to shareholders since 2017. Rountree will remain an adviser through 2027. His final investor presentation also offered a clear message: for now, management sees better opportunities in fee-based insurance businesses and electrical contracting than in assuming additional underwriting risk.

***

Coverager’s upcoming MGA report includes regulatory filing data on Bamboo. Per statutory filings, Bamboo reported MGA premiums written on behalf of Sutton National Insurance Company of $589.8 million in 2025, up from $441.5 million in 2024, $199.2 million in 2023, and $66.6 million in 2022. Bamboo also reported $98.3 million written on behalf of Incline Casualty Company and $8 million on behalf of Accredited Specialty Insurance Company in 2025 — both new relationships for the year — bringing filed MGA premium across the three carriers to roughly $696 million, against the $766 million in managed premiums White Mountains cited in its presentation.