Life360 expands partnership with Arity, pursues Credit Karma’s insurance strategy

Life360 held its FQ2’24 earnings call on August 8, 2024, led by co-founder and CEO Chris Hulls. Key highlights:

- Life360 reported a 20% year-on-year increase in Q2 revenue, reaching $84.9 million. The company’s free member base grew by 4.3 million monthly active users, totaling 70.6 million, a 31% increase from the prior year.

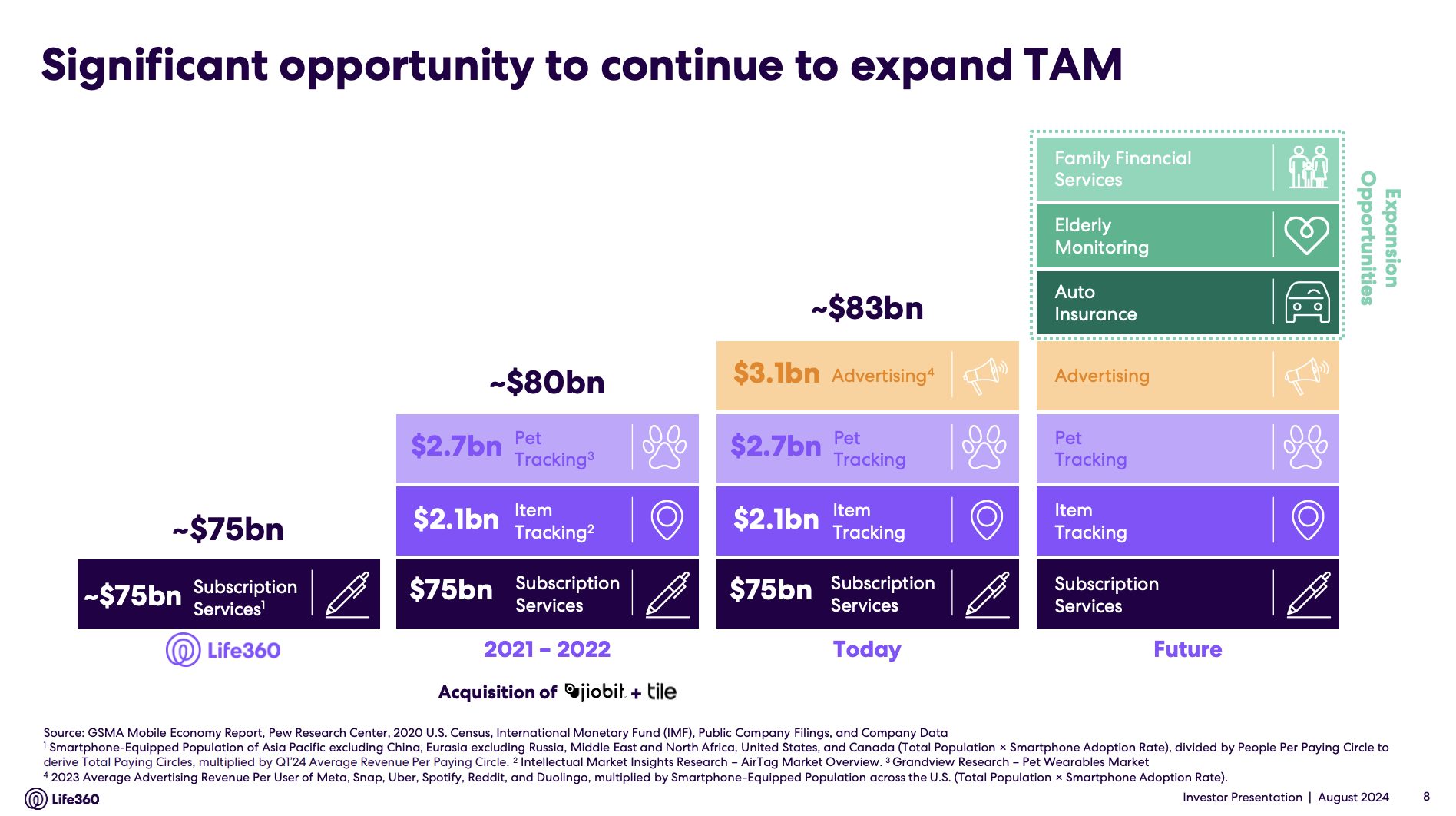

- Life360 launched a new advertising offering in the US in early 2024, now expanding globally. “We continue to expect a noticeable revenue contribution from ads in the second half of 2024, as we build our ad sales, measurement and tech capabilities, and further enable our platform through service integrations like those in place with The Trade Desk, LiveRamp, PubMatic and Google Ad Manager,” said Hulls.

- The company also announced expanded partnerships with Arity and Placer.ai to enhance advertising efforts, leveraging technology for crash detection, driving alerts, and personalized car insurance quotes. “Arity will now become more involved as a contributor to our advertising business going forward, both on-site and off-site, which we’re really excited about.”

- Life360 uses Arity’s technology to enable features like drive detection and crash detection within its app, while allowing Arity to use anonymized location data from the app to generate traffic and transportation insights. These insights are never linked to personally identifiable information. Arity sells these aggregated insights to organizations such as state Departments of Transportation and insurance companies, helping them understand transportation-related trends, like identifying dangerous intersections or road segments.

- Q2 gross profit reached $63.6 million, a 16% year-on-year increase, while adjusted EBITDA was positive for the seventh consecutive quarter, rising to $11 million. Life360 revised its 2024 outlook, expecting consolidated revenue between $370 million and $378 million, with core subscription revenue growth of 25% year-over-year. Adjusted EBITDA is projected at $36 million to $41 million, with an EBITDA loss of $8 million to $13 million, including IPO-related costs.

- The CEO emphasized the company’s long-term vision to evolve beyond simple banner ads and become a platform where users are matched with offers tailored to their data. He highlighted the potential of car insurance as a key example, where Life360 could provide real-time insurance quotes based on users’ driving data, building trust by transparently showing how users rank among other drivers. Hulls referenced Credit Karma’s successful model of using sensitive user data, like credit scores, to match users with credit cards, generating significant lead generation revenue. He noted that Credit Karma is now attempting to replicate this model in the car insurance sector through its acquisition of Zendrive , a direction Life360 is also interested in pursuing. “And with a meaningfully smaller user base than us, they were able to generate over $1 billion of lead-gen revenue. And they actually now are trying to replicate that in the car front, not in a competitive way, but they just bought a company called Zendrive to do exactly what we would like to do in the long run with insurers.”

- Hulls believes that with a highly engaged audience and proprietary first-party data, Life360 has numerous opportunities, such as offering home security and pet insurance based on user behaviors. He sees these offerings as natural extensions of the company’s core product, which could lead to substantial growth and success. “You can also imagine like you move to a new home, we can sell you home security or homeowner’s insurance. You get a new pet, you’ll buy our tracker then we’ll sell you a pet insurance policy. There are many of these things that will feel like they’re extensions of our product and that’s when I think we hit the true goldmine.”

Bottom Line: While Hulls’ insurance narrative isn’t new, this report offers a fresh perspective — but our takeaway is less glamorous: “With this move, we’ll see Credit Karma pushing a product rather than pulling in customers.”

Get Coverager to your inbox

A really good email covering top news.Related Posts